by Ken Gunn

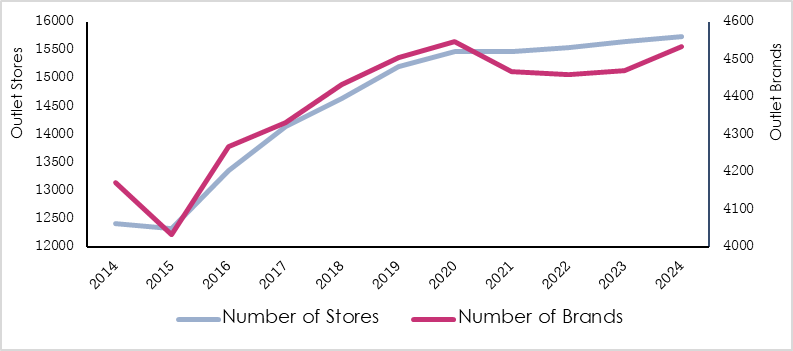

595 new brands entered the European outlet industry in the year. This was 5.1% more than in the year to August 2023 and 2% above the decadal annual average. 531 brands exited the European outlet industry. This was 4.1% less than 2023 and 2% above the ten-year average.

Estate activity amongst established brands (expansion, consolidation or contraction) was 16% greater than in 2023. Stores lost through the contraction of brand estates were outweighed by stores opened through expansion.

The largest recorded number of stores at European outlet centers:

The number of brands has grown across all regions of Europe. However, while Southern and Northern Europe surged by 4.7% and 3.9% respectively, Western and Central Europe saw weaker growth of just 0.6% and 0.5%. Patterns of growth continue to be driven by geopolitical events, uneven economic growth, technological change and a development pipeline which has been constrained by inflated construction costs and high interest rates. Within Europe’s largest markets, Spain, The United Kingdom, Russian Federation and Germany increased brands and stores, Italy increased stores but the Netherlands, Poland and France reduced both brands and stores.

The number of brands with more than 20 outlet stores has grown by 5 to 125 and these account for 13.0% more stores than in 2019, suggesting gradual standardisation of centre propositions. Outlet estates of more than 20 stores now represent 3% of brands and 34.2% of stores, compared to 2% of brands and 24% of stores in 2014, indicating the success of outlet operators in recohnising and cultivating the strongest performing brands.

Brand mix continues to evolve, with 0.6% fewer Clothing & Footwear stores than in 2023, as brands targetting families and older consumers reduced their store count by 3.1% and 7.4%. This was balanced by a rise of 1% in the number of stores serving the outlet industry’s core fashion buyers and a rise in stores providing non fashion (particularly Specialist food and F&B) of 2.9%.

The table below shows that Casual Fashion and Athleisure dominates the Top Thirty European outlet brands. Ken Gunn Consulting multiplies the location of each store in an outlet estate by the specific quality of individal sites (represented by its broad performance tier) to create a ranking of European Brands by Total Brand Mass (TBM). Average Brand Quality (ABQ) is a brand’s total Brand Mass divided by it’s number of stores, and the average ABQ for all European brands is 4.2.

European outlet industry: The Top Thirty Brands

| Rank (EUR) | Brand | Origin | Outlets in Europe | Total Brand Mass | Average Brand Quality | Unit Change 2023/24 | Rank Change 2023/24 | |

| 1 | Levi’s | US | Clothing and footwear | 137 | 569 | 4.2 | 2 | 0 |

| 2 | Guess | US | Clothing and footwear | 137 | 556 | 4.1 | 8 | 0 |

| 3 | Adidas | DE | Leisure | 131 | 498 | 3.8 | 0 | 0 |

| 4 | Tommy Hilfiger | US | Clothing and footwear | 109 | 490 | 4.5 | 7 | 2 |

| 5 | Puma | DE | Leisure | 126 | 487 | 3.9 | 5 | 0 |

| 6 | Lindt & Sprungli | CH | Food | 111 | 475 | 4.3 | 6 | 3 |

| 7 | Calvin Klein | US | Clothing and footwear | 102 | 461 | 4.5 | 6 | 1 |

| 8 | Nike | US | Leisure | 121 | 461 | 3.8 | -2 | -4 |

| 9 | Home & Cook | IT | Household | 111 | 423 | 3.8 | -5 | -2 |

| 10 | Skechers | US | Clothing and footwear | 106 | 407 | 3.8 | 9 | 1 |

| 11 | Boss | DE | Clothing and footwear | 82 | 406 | 5.0 | 0 | -1 |

| 12 | Lacoste | FR | Clothing and footwear | 76 | 385 | 5.1 | 3 | 0 |

| 13 | Timber-land | US | Clothing and footwear | 67 | 346 | 5.2 | 0 | 0 |

| 14 | Sunglass Hut | US | Personal | 69 | 343 | 5.0 | 3 | 1 |

| 15 | Samso-nite | US | Personal | 65 | 332 | 5.1 | 2 | -1 |

| 16 | Under Armour | US | Leisure | 70 | 325 | 4.6 | 10 | 6 |

| 17 | Le Creuset | FR | Household | 66 | 324 | 4.9 | 3 | 1 |

| 18 | Karl Lagerfeld | FR | Clothing and footwear | 54 | 314 | 5.8 | 1 | -2 |

| 19 | New Balance | US | Leisure | 65 | 313 | 4.8 | 0 | 1 |

| 20 | Polo Ralph Lauren | US | Clothing and footwear | 47 | 293 | 6.2 | -1 | 1 |

| 21 | Asics | JP | Leisure | 61 | 288 | 4.7 | -5 | -3 |

| 22 | Gant | US | Clothing and footwear | 62 | 285 | 4.6 | -3 | 2 |

| 23 | Desigual | ES | Clothing and footwear | 73 | 283 | 3.9 | -7 | -6 |

| 24 | Michael Kors | US | Clothing and footwear | 46 | 282 | 6.1 | 4 | 2 |

| 25 | North Face, The | US | Leisure | 47 | 281 | 6.0 | 6 | 4 |

| 26 | Villeroy & Boch | DE | Household | 53 | 280 | 5.3 | -3 | -3 |

| 27 | Jack & Jones | DK | Clothing and footwear | 76 | 273 | 3.6 | 12 | 9 |

| 28 | Swarovski | AT | Personal | 48 | 272 | 5.7 | 10 | 10 |

| 29 | Cosmetics Co. Store | US | Personal | 49 | 266 | 5.4 | 5 | 5 |

| 30 | Geox | IT | Clothing and footwear | 61 | 263 | 4.3 | -3 | -5 |

While Levi’s retains its position as Europe’s leading brand, Guess has narrowed the gap growing by eight stores over the last twelve months. Both brands now have 137 stores but Levi’s has been marginally better at picking stronger locations. Adidas is third but is being pressed by Tommy Hilfiger which has fewer stores but superior locations.

Many brands, particularly those with larger estates, continue to adjust their estates to drive profitability. Puma for example has opened nine stores in the last year, but has also closed four.

Swarowski is the highest climber in the Top Thirty ranking, adding ten stores (including Sicilia FV, La Reggia DO and Seville FO) and rising ten places. Jack & Jones and Under Armour have also been very active, rising nine and six spots respectively.

For the first time in a decade, Nike has not opened a new store at a European outlet centre. The brand has retreated from first place in the 2021/22 ranking with 140 stores, to eight place in 2023/24, albeit, where absent, they still remain at the top of all asset leasing strategies.

Outside the Top Thirty brands, Rituals stepped up expansion from five openings in 2022/23 to fourteen in 2023/24, including Caledonia Park, Hede Fashion Outlet and Marques Avenue Romans. An ABQ of 6.2 indicates a focus on Tier 1, 2 and 3 locations, where Rituals’ affordable luxury products for home and body (ideal as treats and gifts) align strongly with outlet guest aspirations.

Jack & Jones opened eighteen stores in 2022/23 and thirteen stores in the most recent year. Targeting the Young lifestage, the Bestseller Group owned menswear brand added seven stores in Central Europe and now has 76 outlets and now ranks 27th amongst European outlet brands. Other brands in the Bestseller stable have also expanded, with Only adding ten stores, Name It seven stores and Only & Sons six stores. In total, Bestseller brands have added 35 stores and increased their presence in European outlets by 29% this year.

Elsewhere, Betty Barclay Group brand Zero has made a strong return to the outlet industry after an eight-year hiatus. Zero has acquired nine sites in Germany, including Zweibrücken Fashion Outlet and Designer Outlet Neumünster.

The Top Thirty Outlet Centres 2024 : Stable at the top but challengers below

| 2024 Rank | Centre Name | Country | Brand Mass (TBM) | Brand Quality (ABQ) | Change in Rank vs 2023 | Change in TBM 2023/24 | Change in ABQ 2023/24 |

| 1 | Bicester Village | GB | 1,486 | 9.2 | 0 | 1% | 1% |

| 2 | Serravalle DO | IT | 1,346 | 5.8 | 0 | 2% | 0% |

| 3 | Roermond DO | NL | 1,145 | 5.8 | 0 | -3% | 1% |

| 4 | La Roca Village | ES | 1,084 | 7.6 | 0 | -2% | 0% |

| 5 | Noventa di Piave DO | IT | 974 | 5.7 | 1 | 2% | 1% |

| 6 | DO Parndorf | AT | 969 | 5.6 | -1 | -2% | 0% |

| 7 | Kildare Village | IE | 936 | 7.7 | 2 | 6% | 1% |

| 8 | La Vallee Village | FR | 929 | 8.6 | -1 | 4% | 2% |

| 9 | Foxtown Mendrisio | CH | 898 | 5.5 | -1 | 1% | -1% |

| 10 | Castel Romano DO | IT | 832 | 5.3 | 0 | -1% | 0% |

| 11 | OC Metzingen | DE | 823 | 6.0 | 0 | 2% | 0% |

| 12 | Fidenza Village | IT | 810 | 6.8 | 0 | 2% | 0% |

| 13 | Ingolstadt Village | DE | 779 | 7.0 | 5 | 7% | 3% |

| 14 | Cheshire Oaks DO | GB | 773 | 5.0 | 1 | 0% | 0% |

| 15 | Sicilia FV | IT | 738 | 4.6 | 9 | 18% | -2% |

| 16 | Wertheim Village | DE | 731 | 6.5 | -3 | -8% | 0% |

| 17 | Vnukovo OV | RU | 721 | 4.2 | 2 | 2% | 0% |

| 18 | Maasmechelen Village | BE | 714 | 7.0 | -4 | -8% | -1% |

| 19 | Las Rozas Village | ES | 708 | 7.6 | 1 | 1% | 4% |

| 20 | La Reggia DO | IT | 694 | 4.4 | -4 | -1% | -1% |

| 21 | Belaya Dacha OV | RU | 681 | 4.0 | -4 | 1% | -1% |

| 22 | Valmontone Outlet | IT | 668 | 3.7 | -1 | 1% | 1% |

| 23 | Franciacorta OV | IT | 635 | 4.1 | -1 | -1% | -1% |

| 24 | Gunwharf Quays | GB | 633 | 4.9 | -1 | -2% | -2% |

| 25 | DO Neumunster | DE | 622 | 5.0 | 2 | -1% | -2% |

| 26 | The Village | FR | 618 | 4.8 | 0 | -2% | -2% |

| 27 | FO Lisbon | PT | 605 | 4.8 | 4 | -1% | 0% |

| 28 | Batavia FO | NL | 603 | 4.8 | 0 | -6% | 0% |

| 29 | Barberino DO | IT | 580 | 4.6 | -4 | -5% | -2% |

| 30 | Novaya Riga | RU | 578 | 3.7 | 5 | 8% | -3% |

Brand demand is the key determinant of asset performance and there are 210 outlet centres in the European outlet industry today. These can be ranked by summing the individual ABQ’s of every brand present, a metric which explains c. 92% of the variance in turnover. As mentioned earlier, it is almost impossible to break into the leading assets given their size and maturity, so the sites in the Top Ten are the same as last year, with only minor changes in position.

Outwith the Top Ten, there have been more substantive changes, with this year’s standout improvement at Sicilia Fashion Village. The opening of a 6,000 sq m extension in June has increased TMB by 18% and elevated the asset nine places, to 15th spot in the ranking.

Other notable performers include Ingolstadt Village, which has seen significant remerchandising activity over the past two years and Moscow’s Novaya Riga Outlet Village which was expanded in late 2023.

It is important to recognise the hard work over many years and success achieved this year throughout the outlet community. The table below shows the top climbers in the ranking, outside the Top Thirty assets.

The operational nature of outlet assets encourages continuous improvement

| 2024 Rank | Centre Name | Country | Brand Mass (TBM) | Brand Quality (ABQ) | Change in Rank vs 2023 | Change in TBM 2023/24 | Change in ABQ 2023/24 |

| 80 | Seville FO | ES | 307 | 4.5 | 27 | 21% | 3% |

| 87 | DO Algarve | PT | 279 | 4.2 | 22 | 12% | 2% |

| 170 | FH – Pallady | RO | 112 | 2.7 | 20 | 55% | 10% |

| 154 | Outleto | BY | 141 | 2.0 | 18 | 24% | 1% |

| 116 | Oslo FO | NO | 225 | 3.9 | 14 | 14% | 0% |

| 75 | Brugnato 5Terre OV | IT | 318 | 3.5 | 13 | 14% | 1% |

| 92 | O2 Outlet | GB | 268 | 3.8 | 12 | 6% | -3% |

| 63 | DO Ochtrup | DE | 342 | 4.3 | 11 | 5% | -2% |

| 82 | Citta Sant Angelo OV | IT | 302 | 3.4 | 11 | 12% | 1% |

| 109 | The Mall Sanremo | IT | 246 | 9.1 | 11 | 18% | 1% |

| 121 | Brands Stories OC | RU | 210 | 3.4 | 11 | 11% | 0% |

| 118 | DO Croatia | HR | 223 | 3.5 | 10 | 12% | -2% |

| 15 | Sicilia FV | IT | 738 | 4.6 | 9 | 18% | -2% |

| 91 | One Salonica | GR | 269 | 3.5 | 9 | 6% | 1% |

| 130 | Coruna – TSO | ES | 187 | 3.6 | 9 | 2% | 0% |

| 135 | XL Family Outlet | RU | 180 | 2.6 | 9 | 11% | -1% |

| 152 | Hanse Outlets | DE | 145 | 3.7 | 9 | 11% | 0% |

| 65 | Szczecin O Pk | PL | 340 | 2.6 | 8 | 4% | -1% |

| 70 | Roubaix DO | FR | 324 | 4.2 | 8 | 6% | 2% |

| 104 | Hede FO | SE | 253 | 4.0 | 8 | 7% | 0% |

| 114 | Outlet Aubonne | CH | 229 | 4.4 | 8 | 10% | 2% |

| 123 | Torre Village | ES | 207 | 3.2 | 8 | 8% | 1% |

| 39 | DO Salzburg | AT | 477 | 4.4 | 7 | 13% | -1% |

| 44 | Swindon DO | GB | 451 | 4.2 | 7 | 15% | 0% |

| 72 | W Midlands DO | GB | 323 | 4.4 | 7 | 7% | 0% |

| 108 | Sambil Madrid | ES | 246 | 3.0 | 7 | 11% | -1% |

| 139 | Campera SV | PT | 172 | 3.3 | 7 | 5% | -1% |

| 54 | Mallorca FO | ES | 377 | 4.6 | 6 | 4% | -1% |

| 88 | Junction 32 | GB | 275 | 3.3 | 6 | 4% | 0% |

| 117 | Brennero DO | IT | 223 | 3.8 | 6 | 9% | 3% |

Following the opening of a 3,800 sq m extension in November 2023, Seville Fashion Outlet is this year’s highest climber, rising twenty seven places.

Designer Outlet Algarve (PT) is also expanding, with a second phase of 4,000 sq m underway and improvement of twenty-two places this year.

Fashion House Pallady opened a second phase of 5,724 sq m in June, achieving 55% growth in TBM, and impressive 10% increase in ABQ and a rise of twenty places. Footfall is reported to be up 30% since the extension.

Elsewhere, relatively recent outlet developments continue to mature. For example, the O2 Outlet in London saw a net increase of six brands, which increased TBM by 6% and improved it’s ranking by twelve places). The Mall Sanremo added six luxury brands, disposed of two, improved TBM by 18% and rose eleven places in the ranking. West Midlands DO increased TBM by 7% and climbed seven places, with a future extension.

However, growth is not limited to newer sites. Many outlet centres have improved as short lease lengths, which encourage sales growth, backed by appropriate funding from investor partners have conspired to maintained fresh, relevant brand offerings. For example, while Hede Fashion Outlet is 25 years old, Swindon Designer Outlet is 27 and Campera Shopping Village is 24, they have each climbed at least seven places in this year’s ranking, and outperformed many younger assets. The skill and capabilities of today’s operators are widely publicised but they also have the advantage of being able to build on the hard work and good (brand enhancing) designs of the past. An important lesson for those tempted to think that outlet will easily work in redundent or compromised spaces.

The European outlet industry is in great shape and looking forward to another strong year of sales and revenue growth. Prospects for the longer term are excellent, and will be driven by brands seeking turnover growth, consumers seeking superior brand experiences and investors seeking growth in income. These goals align perfectly and this year’s performance shows that the powerhouse partnership at the heart of outlet centre operations is not only stronger but more ambitious than ever.

Ken Gunn

Ken Gunn is the Managing Director of Ken Gunn Consulting.