In recent years, the dynamic of shopping centers has shifted, from retail hubs to entertainment and social places, driven in part by the decline of major physical brands and department stores, the conversion of retail space for other purposes, and the rise of experiential propositions.

Underlying drivers of change, such as ESG, an aging population, the emerging demands of Gen Z, cost of living challenges, and hastening digital innovation, have the potential to either be a tailwind or headwind for shopping centers, depending on how prepared they are.

Indeed, shopping center investors and managers are increasingly concerned about the role of their assets, the value and experience they deliver, and how they can resonate in a digital age.

The overriding focus for shopping centers in 2024, continues to be renewal and adaptation.

While potential solutions will vary, we can be certain they will require strong market intelligence, especially timely and accurate insights into the behaviors of the people who use, or might use, shopping centers.

The Role of Catchment Insight

Consumer and catchment insights are vital factors in shopping center decision making. Those insights help occupiers understand the volume and value of their target audiences, marketers define who and how best to target, investors assess the suitability of assets within their portfolios, and developers and asset managers identify opportunities for new propositions or challenges with oversupply.

Until recent times, the shopping center sector relied on a mix of aging and static information to help navigate the complexities of asset decisions. However, digital technology and data are transforming the game, allowing us to tap into faster and deeper insights, answer critical questions more effectively, and unlock the potential of retail spaces with greater confidence.

Current State

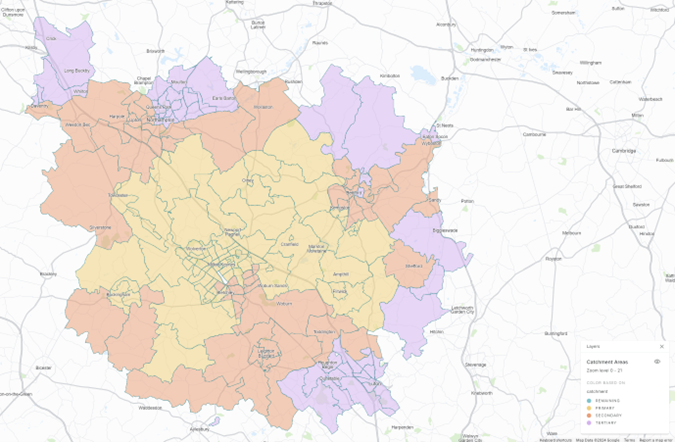

Catchment analysis, the process of understanding consumer geographical demand and socio-demographic profiles, has long influenced the retail asset decision-making process. However, traditional catchment analysis has always been a blunt tool. Defined using historical shopping patterns as well as demographic and expenditure estimates, it typically offers no more than a high-level and static window into consumers, their broad residential locations, and their presumed attraction to and visitation of retail destinations.

The key limitation of catchment analysis is a tendency to over rely on historical consumer data, meaning it, at best, provides an approximate understanding of dynamic behaviors. As consumer behavior becomes more complex, there is a greater need for shopping centers to answer more nuanced questions, such as how and why consumers use destinations, as well as the true impact of online channels. Consequently, many stakeholders are re-evaluating their approach to how consumer demand and catchment area insights are collected, analyzed, and leveraged.

Recent Developments

With “adaptability” something of a byword in the industry, there is sharpened focus on using new data sources to understand the changing needs of people.

There is a burgeoning market for third-party insights, which shopping centers can tap into to generate unprecedented empirical observations about people and how they use spaces.

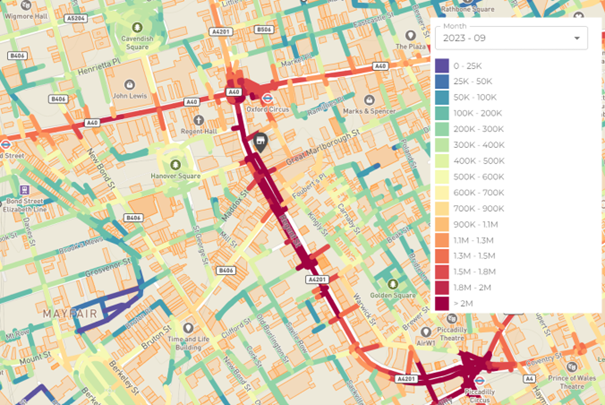

For example, anonymized consumer mobility data, derived from mobile phone movement, has rapidly disrupted this staid area, offering detailed insight into the types of people who utilize shopping centers on different days and times of the day, including how often they frequent and dwell in those places. These massive and trending data sets are increasingly used to calibrate catchment area models, increasing their accuracy and applicability.

At a localized and granular level, telcos can provide people movement at just five meters, through spaces, 24 hours a day, 365 days a year. That allows for the micro-analysis of behavior within shopping centers, which is key to predicting use within and around retail spaces.

Consumer expenditure insights, derived from financial data providers, are adding another layer of insight, providing a trending view of patterns of geographical spend by categories, such as Clothing & Footwear, Homeware, and Food & Beverage.

Furthermore, innovations in the depth and speed of demographic insights are offering new ways to understand the needs of people at the local level. For example, geosocial data, based on analyzing anonymized social media conversations across different consumer segments by geography, are increasingly providing a better understanding of trending lifestyle choices.

There is also greater recognition of the importance of shopping centers collecting their own first-party data. The use of loyalty schemes (for example), administered through apps and websites, not only allows shopping centers to directly engage consumers, but to also benefit from the behavioral insights such tactics can generate.

While quantitative data tells us what people do in catchments and shopping centers, it does not help us understand “the why”. There remains a crucial need to also understand the attitudes and wants of people. Surveys of the sentiments, preferences, and perspectives of people are nothing new, but technology is making it easier to gather those insights.

Various platforms offer on-demand access to target audiences, allowing shopping centers to understand how people feel, think, act, buy, and interact with locations and types of spaces.

Traditionally an expensive form of research, accurate insights can now be gained within hours from diverse and representative audience panels, at modest cost. That allows stakeholders to develop greater empathy with the users of spaces, driving better and more human-centric decisions.

Real-world Examples:

Looking toward the future, the capability to harness real-time data feeds, from sources such as social media and footfall, will ensure AI is likely to become a powerful tool for the identification of emerging consumer trends and behaviors. That has the potential to transform decisions about the use and branding of retail locations, tenant mix, and strategies for maximizing commercial returns from shopping centers.

Finally, as more data about people is collected, the application of generative AI will likely become feasible. For example, it is conceivable (with the right data) that we will be able to test questions such as “How would a suburban family segment react to a new retail concept?” at speed and far more cheaply than conventional research allows.

Shopping center analysts are starting to blend traditional and innovative data sources to answer key questions.

Use Case: Assessing Untapped Demand

A key question asked by shopping centers is: To what degree actual performance meets the potential of a catchment?

Major landlords are answering this question by blending data from various quantitative sources. Details include turnover data (provided as part of turnover leases) to understand center performance, catchment areas derived from mobile data to provide a current view of geographical demand, and financial data to provide a trending view of who spends what by product category, where, and when.

When coupled with qualitative surveys, focused on consumer sentiment, shopping centers can complement the “what” of consumer behavior, with the “why” behind choices.

It can help address questions such as:

- In what categories does the center over perform?

- In what categories does the center underperform?

- Where is there a performance gap; what is the potential size of prize?

- What categories are likely to be most acceptable to consumers?

- Are there knowledge blind spots, such as spend being diverted to online players (e.g., Netflix, Deliveroo, or Depop), which will help us better respond to online competition?

This blended approach is developing quickly and is helping shopping centers address questions that would have been difficult to answer as little as three years ago.

Use Case: Demonstrating Impact

Another common question asked by shopping centers is: What is the impact of key initiatives?

The new wave of consumer mobility, financial, and first-party data collected by shopping centers is significantly improving the accuracy and timeliness of analysis, due to the unprecedented detail such data provides into the behavior of different types of consumers at specific locations at specific times.

This is driving improvement in how the impacts of actions and initiatives are measured, with respect to their influence on consumer behavior.

Real examples include:

- Where a new flagship store has opened in a former department store, this analysis has been used to assess how much further a shopping center reaches into its catchment area, how market share has changed, and which types of consumers this change resonates with the most.

- The effectiveness of a marketing campaign targeted at luxury shoppers was measured in terms of penetration into specific catchment postcodes, and subsequent changes in KPIs, such as visit footfall, dwell, spend, and long-term shopper value.

Going Forward

As shopping centers continue to navigate the evolving retail landscape, it is clear that data continues to be the gateway to better consumer and catchment insights. It offers new opportunities for understanding people, developing strategies, assessing commercial feasibility, designing spaces, and tracking performance.

If innovation is to be sustained, shopping center stakeholders need to develop strong data strategies, founded on clear use cases for consumer data, which answer both the “what” and “why” of consumer behavior.

That requires a purposeful and clearly articulated approach to sourcing and collecting consumer data from a variety of sources, including first-party methods and primary research.

Furthermore, a structured and strategic approach to high-quality, high-volume, and high-variety data is a precondition of smarter advanced analysis, including the various opportunities offered by artificial intelligence.

Ultimately, better data and analytics will help put you on the right side of consumer trends, which will only continue to influence the purpose and performance of our shopping centers.

James Miller

James Miller is the Director of Pragma Consulting