- Global Retail Attractiveness Index bounces back after sharp drop in second quarter of 2020

- Germany tops GRAI ahead of Czech Republic and Ireland despite losses

- Denmark the only market to grow thanks to high consumer confidence

- Austria and Portugal suffered the heaviest losses in the retail index over the year, each declining by 21 points

- Canada ranks lowest of all 20 countries surveyed

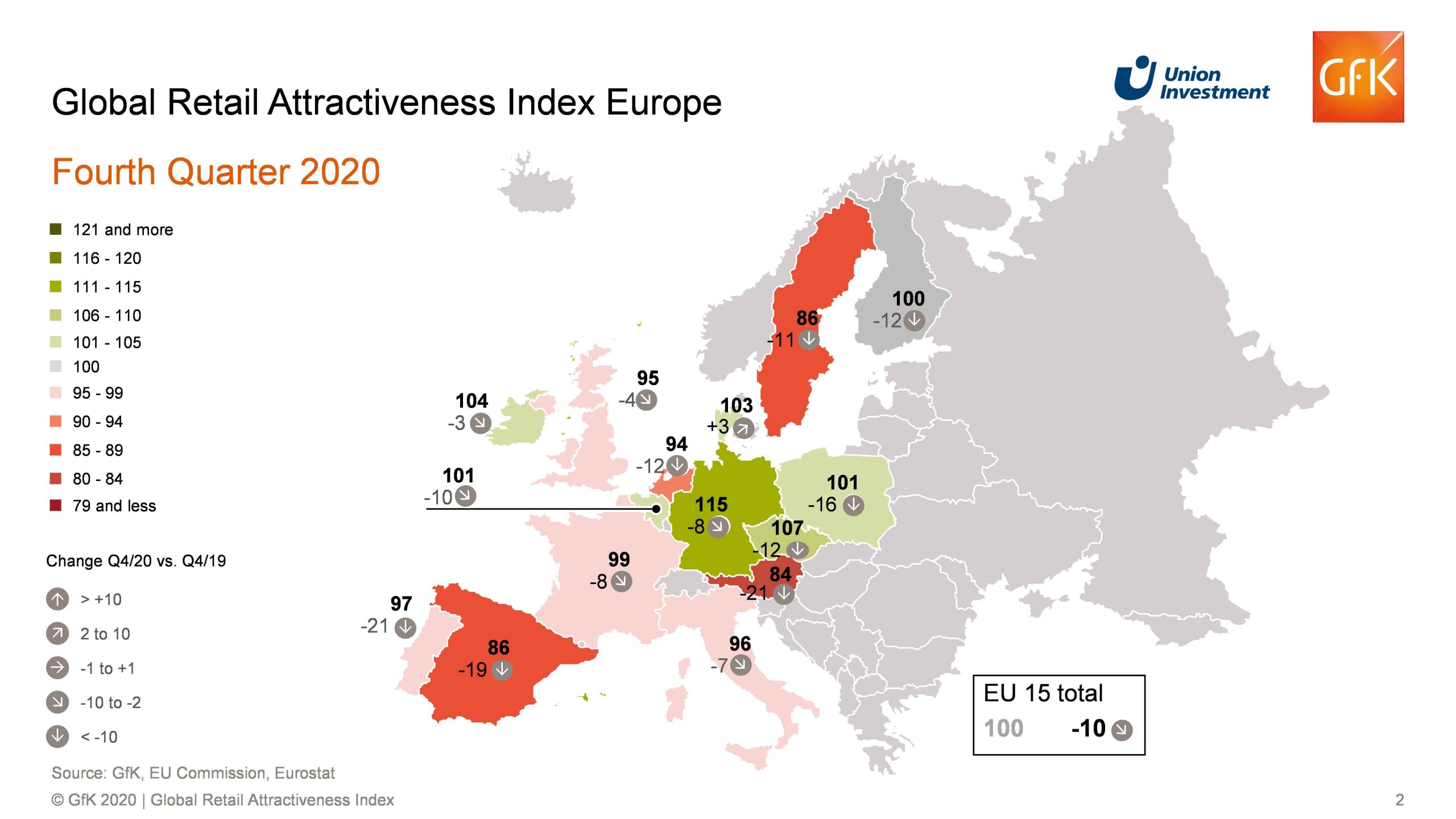

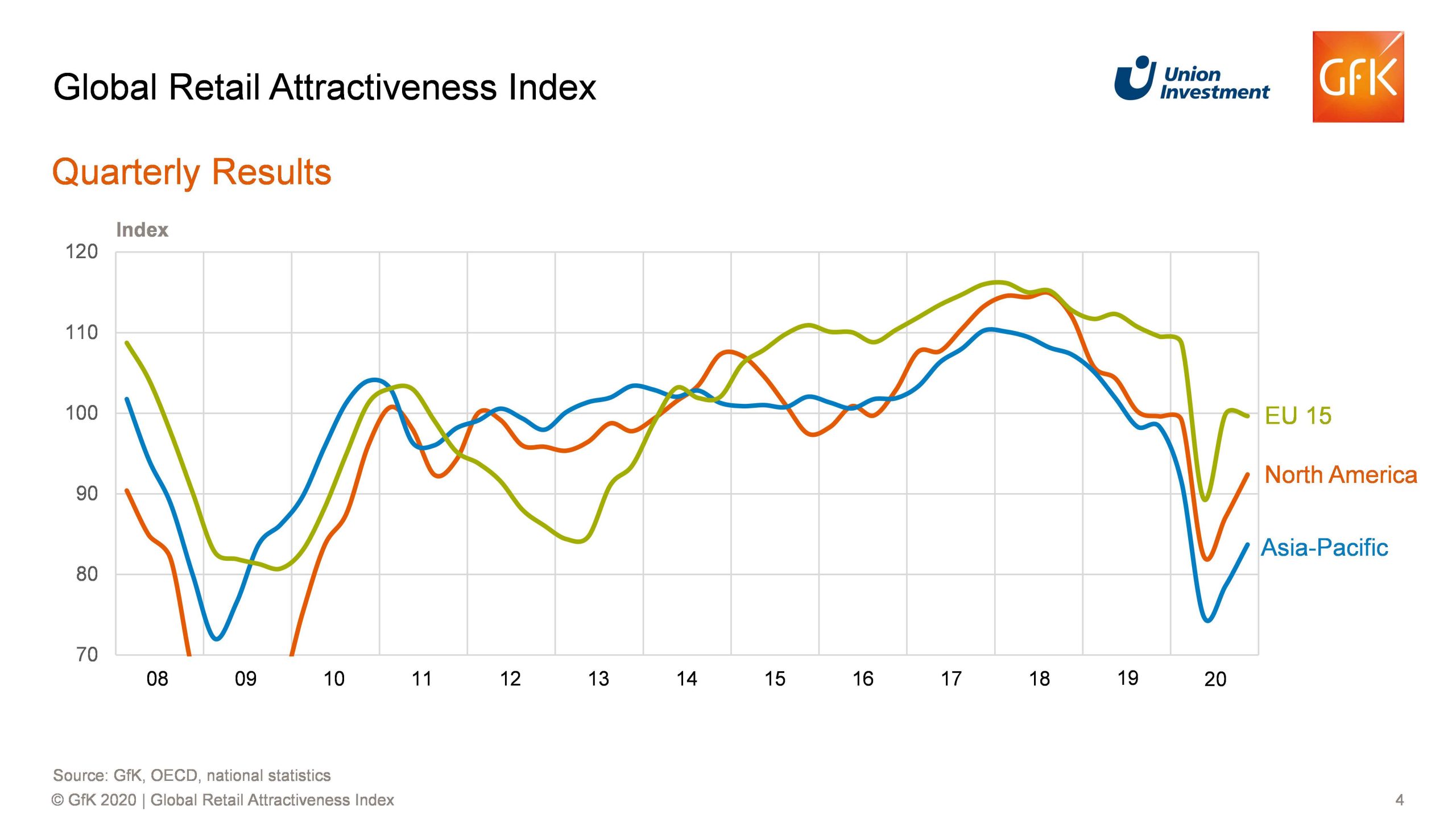

The first Europe-wide lockdown in spring 2020 sent retail markets from Scandinavia to the Iberian peninsula into an unprecedented state of collective shock. This was reflected in the European retail industry barometer, the Global Retail Attractiveness Index (GRAI), which plummeted to a historic low of 89 points in the second quarter. A deeper crash appears to have been avoided, though. That is the conclusion reached by GfK and Union Investment, who have been compiling the GRAI for 20 countries worldwide since 2017. Despite retailer and consumer sentiment remaining stuck in the coronavirus trough, the rapid return of the GRAI (EU-15 Index) to 100 points in the fourth quarter of 2020 suggests that the steep decline has come to an end.

The negative trend was offset for the time being by the labour market, which held up well in many parts of Europe in the fourth quarter and was the strongest performer of the four GRAI indicators, at 123 points. France, Italy, the Netherlands and Belgium in particular did well on this front. The retail sales trend (105 points) was likewise supportive. In 10 of the 15 countries surveyed, sales showed an upward trend. Overall, however, the GRAI in Europe remains ten points below the prior-year level.

“Sentiment in the retail sector and also among consumers is currently holding the retail index back,” said Henrike Waldburg, head of Investment Management Retail at Union Investment. Having posted significant losses over the year of minus 26 and minus 16 points respectively, the two GRAI sentiment readings were well below average at 89 and 85 points. It’s also important to note that the labour market is a lagging indicator. “An ongoing recession with rising unemployment figures is likely to impact the index going forward,” commented Henrike Waldburg.

Resilience in the crisis

The German retail market performed surprisingly well in the fourth quarter and bucked the wider trend. With 115 points (minus eight points compared to Q4 2019), Germany remains the clear leader in a struggling field. The leading trio in the fourth quarter of 2020 are now Germany, the Czech Republic (107 points) and Ireland (104 points). Denmark (103 points), Belgium and Poland (101 points each) also have above-average scores on the European retail index. Having said that, the latter country lost a significant amount of ground compared to last year. Austria and Portugal suffered the heaviest losses in the retail index over the year, each declining by 21 points, followed by Spain (minus 19 points). Austria was the worst performer in the fourth quarter, with just 84 points, while Spain and Sweden did only marginally better at 86 points each. Buoyed by strong consumer optimism and positive retail sales performance, Denmark was the only European country in the EU-15 Index to improve slightly year-on-year in the fourth quarter, gaining three points.

“Although the second and third lockdowns, increasing consumer concern about jobs, and retailers fearing for their livelihoods in almost all European countries have dragged the retail index down over the course of the year – from minor losses, such as Germany, Ireland and the UK, to significant declines like in Austria, for example – many European retail markets have shown a degree of resilience during the crisis. This is particularly true when compared to international markets such as Japan and Canada, where volatility is currently much higher,” said Olaf Janßen, Head of Real Estate Research at Union Investment.

Crossover concepts offer opportunities

“Transformation is in full swing,” said Henrike Waldburg. “The coronavirus crisis will amplify long-term trends and separate the wheat from the chaff, completely redefining which combination of retail property, retail concept and tenant structure will deserve the label ‘core’ in future. In the strong European markets that pass the crash test, there will also be opportunities for investors in the years ahead, however, including new crossover concepts that bring together retail and other exciting uses.”

Europe leads North America leads Asia-Pacific

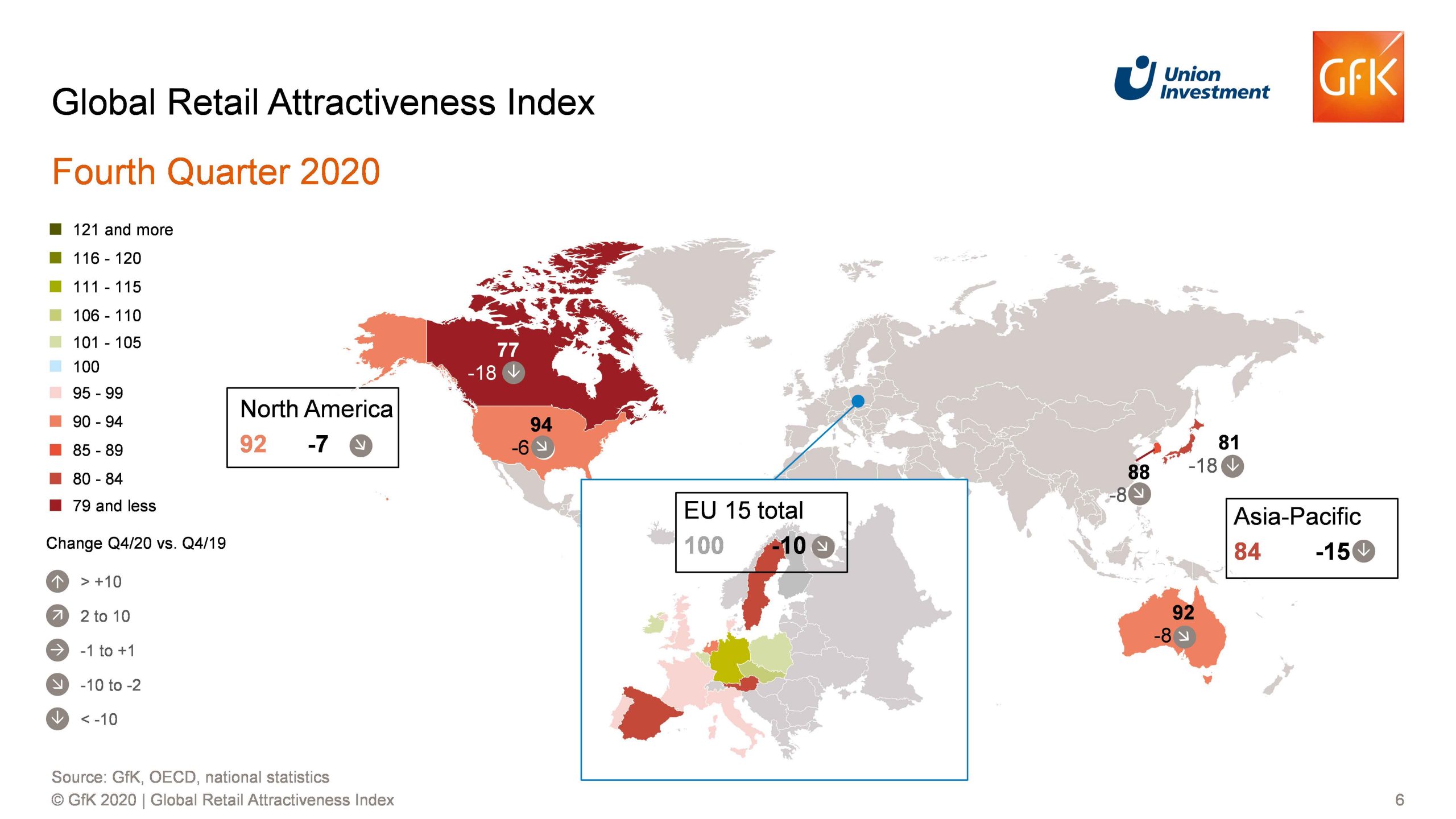

Overall, the European retail index (100 points) remains ahead of the international indices, both in North America (92 points) and in Asia-Pacific (84 points), where the global recession triggered by the pandemic is being felt much more strongly. Compared to Europe (minus ten points), the North America index losses are somewhat smaller (minus seven points). Supported by a strong rise in retailer sentiment, in the US the index suffered only moderate losses but nevertheless came in at a rather weak 94 points. The US was unable to compensate for the negative impact of Canada on the North America Index, with its northern neighbour losing 18 points compared to the previous year. In the fourth quarter of 2020, Canada was still the lowest ranked among all 20 countries covered by the GRAI, with just 77 points.

In the Asia-Pacific region, the GRAI recorded somewhat stronger losses than Europe and North America over the course of the year, totalling 15 points. Japan played a major role here, with all four indicators being down on the last survey. The decline was especially marked with regard to labour market data and associated consumer sentiment.

Methodology

Union Investment’s Global Retail Attractiveness Index (GRAI) measures the attractiveness of retail markets across a total of 20 countries in Europe, North America and the Asia-Pacific region. An index value of 100 points represents average performance. The EU-15 index combines the indexes for the following EU countries, weighted according to their respective population size: Denmark, Finland, Germany, France, Italy, Spain, Sweden, the United Kingdom, Austria, the Netherlands, Belgium, Ireland, Portugal, Poland and the Czech Republic. The North America index comprises the US and Canada, while the Asia-Pacific index covers Japan, South Korea and Australia.

Compiled every six months by market research company GfK, the Global Retail Attractiveness Index consists of two sentiment indicators and two data-based indicators. All four factors are weighted equally in the index, at 25 per cent each. The index reflects consumer confidence as well as business retail confidence. As quantitative input factors, the GRAI incorporates changes in the unemployment rate and retail sales performance (rolling 12 months). After standardisation and transformation, each input factor has an average value of 100 points and a possible value range of 0 to 200 points. The index is based on the latest data from GfK, the European Commission, the OECD, Trading Economics, Eurostat and the respective national statistical offices. The changes indicated refer to the corresponding prior-year period (Q4 2019).