2024 was mostly a period of stabilization for the European grocery sector with the first signs of recovery in some markets. Despite stabilization, 2024 remained a challenging year for European grocers. Economic pressure persisted, which led to cautious consumer behavior as well as restrained spending. Grocery sales grew by 2.4 percent in Europe, slightly above the food price inflation rate of 2.3 percent. Discounters and private labels continued to gain market share, although at a much slower pace than in 2023, largely in line with a longer-term trend observed in previous years. On average, across Europe, there was almost no net effect from up- or downtrading. The 25 percent of consumers who traded up to more expensive options in 2024 were balanced by a similar proportion of consumers trading down—a clear stabilization after two years of strong downtrading.

To thrive in this competitive landscape in 2025, grocers could double down on growth opportunities through differentiation, focus on execution efficiency, meet the needs of the consumer of the future, and leverage data, AI, and technology.

Low Volume Growth Shapes Europe’s Markets

The grocery retail sector experienced low volume growth in 2024. While this trend is expected to continue in the next five years, there are promising signs of potential growth.

Volume growth was low in 2024 (0.2 percent since 2023), and this trend is expected to continue, with up to 0.2 percent volume growth annually through 2030 across Europe. As far as channels are concerned, the shift from traditional trade to modern trade is expected to drive net growth of 0.1 percent annually through 2030, especially in Central and Eastern Europe, as well as Southern Europe. Meanwhile, the shift from grocery to foodservice is expected to lead to a decline in volume of 0.3 percent annually. The largest positive effect is population growth, with a net growth of 0.2 percent annually in Europe, yet negatively impacting Central and Eastern Europe.

Despite low overall growth, there are signs of potential growth in certain channels and categories. Among channels, online is expected to see the highest growth (2.0 percentage points above average), followed by discounters (0.8 percentage points above average). Categories that are expected to grow the most include fresh foods, healthy foods, and functional foods, such as power bars, protein-rich options, and sports drinks. Convenience and food-to-go categories are expected to be major growth pockets, too.

Private Labels Are Gaining Additional Market Share

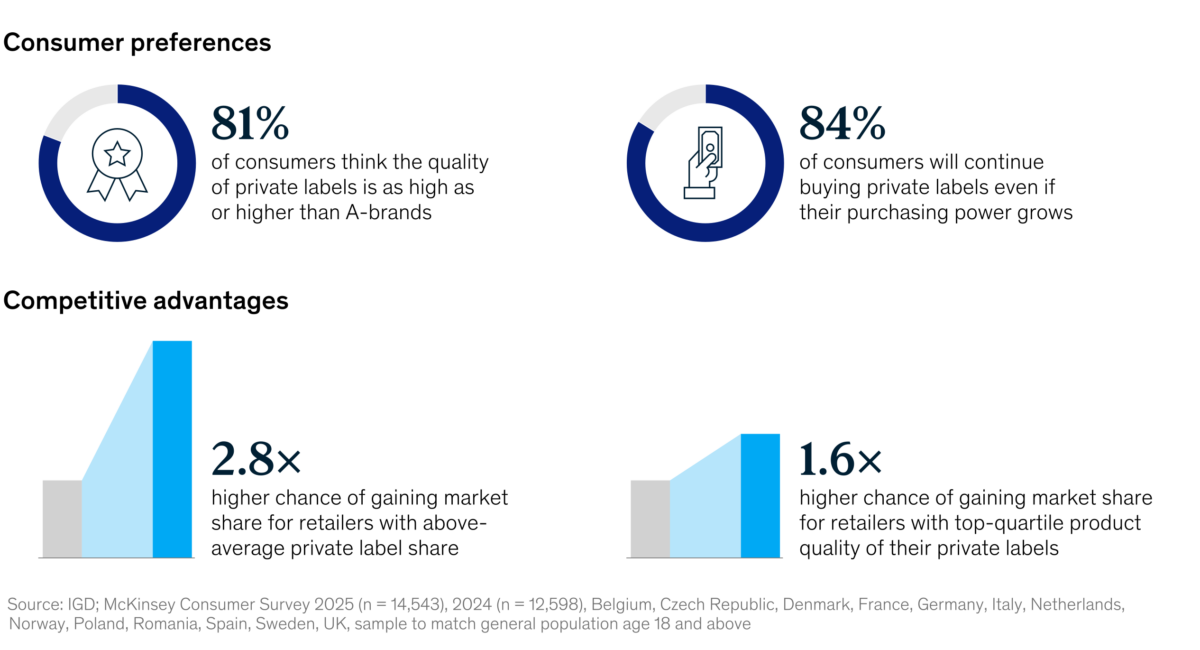

The private label share of total grocery sales value in Europe increased by 0.3 percentage points from 2023 to 39.1 percent in 2024. Although consumer downtrading decreased in 2024, most consumers are not reverting back to A-brands from private labels. In the 2025 survey, 84 percent of consumers say they will continue buying private-label products even if their purchasing power grows.

The sales share of private labels could reach 40.0 to 42.0 percent by 2030, up from 39.1 percent in 2024. The lower end of this range (40 percent) is based on the growth rate observed between 2014 and 2019, while the higher end (42 percent) is based on the growth rate observed between 2014 and 2024.

Private labels are an important driver of market share growth for grocers. The growth champions’ analysis shows that retailers that have an above-average private label share have a 2.8 times greater likelihood of gaining market share than their peers. Those with top-quartile private label product quality have a 1.6 times higher chance than others to gain market share

Grocers who create not just private labels but private brands, similar to A-brands, can gain significant market share. These grocers have established their own product development, concept, design, and packaging departments to differentiate their offering. Rather than adopting cross-category brands, they often use category-specific brands designed to evoke specific emotions and appeal to different customer groups.

Growing Demand For Healthy Food

The demand for healthy options is growing, especially for fresh, functional, and “clean” food. Healthy options and foods that offer additional health-related benefits, referred to as functional foods, are growing rapidly.

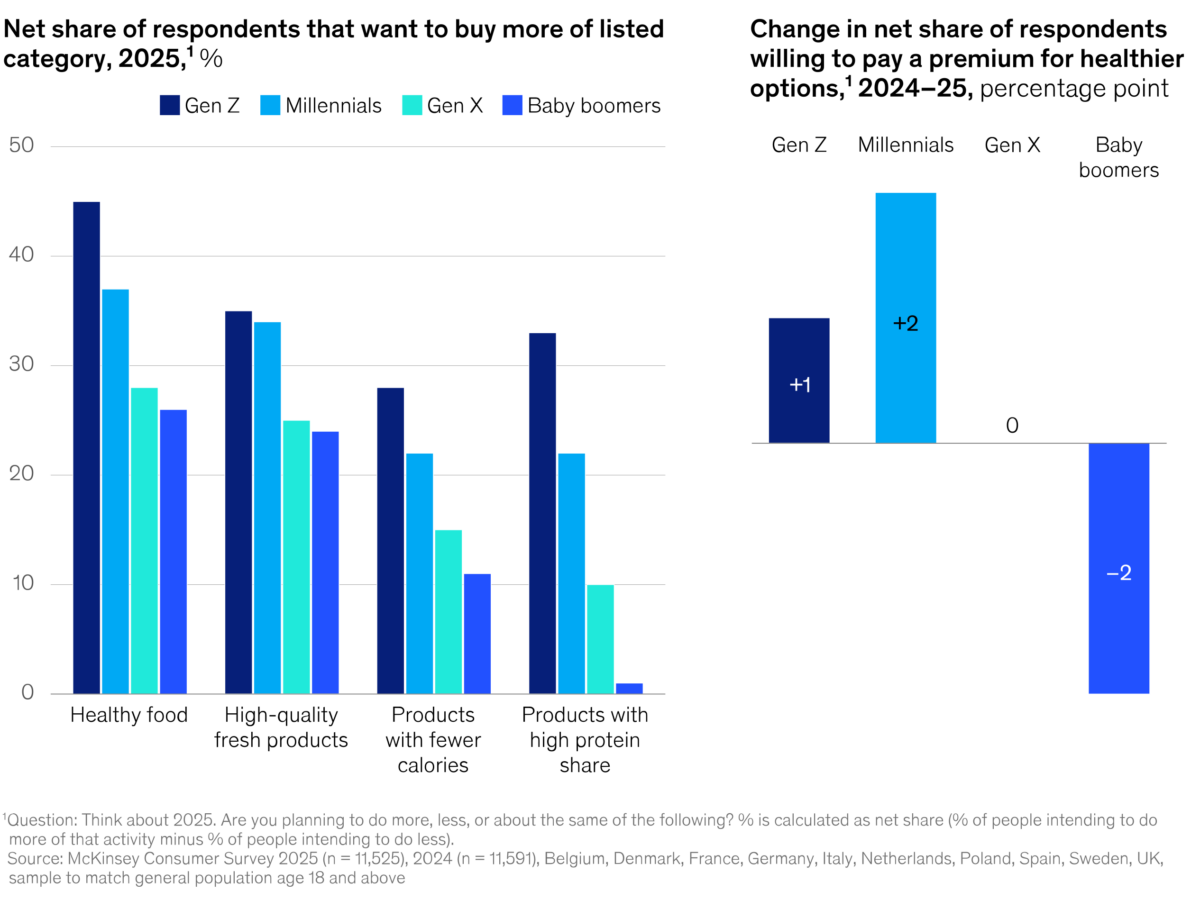

The net intent of European consumers to buy more high-quality, fresh products has increased by two percentage points since 2024. At the same time, some consumers are concerned about certain ingredients that are often found in processed foods.

Gen Z is the group seeking healthy options the most. Gen Z has the highest growth as a group of shoppers, and this group also has the highest intent (45 percent) to focus on healthy nutrition among all cohorts.

Sustainable Products Are Less Enticing For Consumers

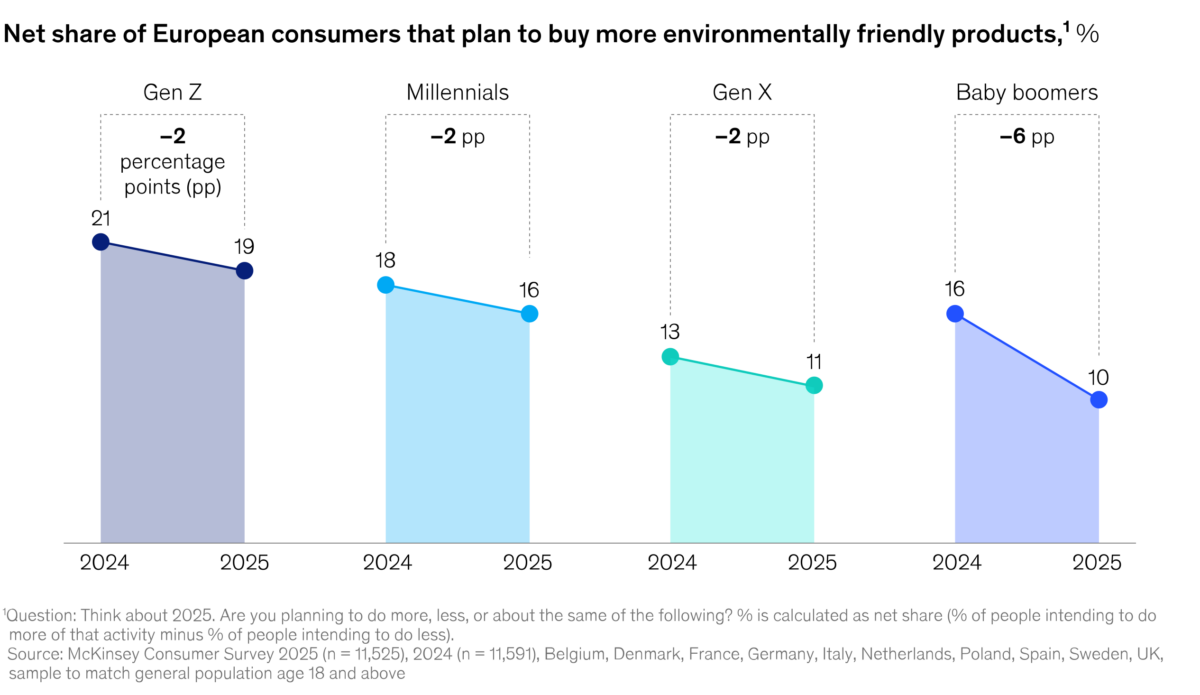

According to the consumer survey, the share of consumers who want to buy products that are more sustainable has decreased. However, Gen Z shoppers and millennials have an approximately 1.8 times greater intent to purchase more sustainable products than Gen X and baby boomers, and their share of the total number of shoppers is increasing

This year, many retailers are focusing on addressing upcoming regulations. In 2025 and 2026, several major sustainability-related directives and regulations are coming into force. Compliance requires significant effort and investment by retailers. At the same time, several grocers have extended the timeframe for reaching their voluntary commitments for various sustainability dimensions, for example recyclable or compostable packaging.

The Race To Get Tech Right

Data, AI, and tech are higher than ever on CEOs agenda as the gap between leaders and late adopters widens.

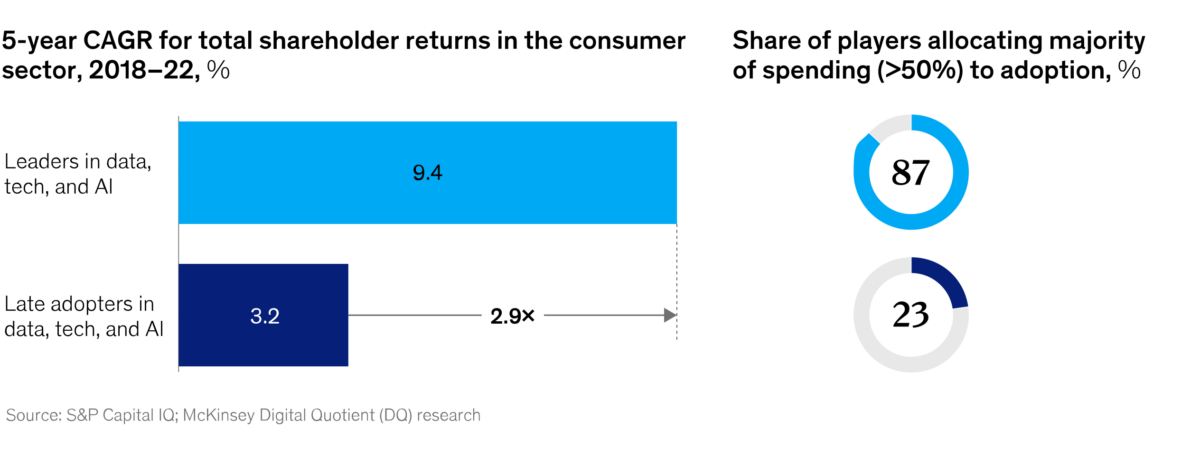

Data, AI, and tech attract increasing CEO attention and capital expenditure. Four years ago, “modernizing IT” and “adopting advanced analytics and AI” were not among the top seven priorities for grocery CEOs. Today, they rank third and sixth, respectively. This shift is reflected in investment patterns: capital expenditure by 19 European grocery sector leaders increased by 13.9 percent between 2021 and 2023, mostly driven by investments in IT, AI, and automation.

The benefits of superior capabilities in data, AI, and tech are substantial. McKinsey’s research shows that retail and consumer goods companies that have above-average capabilities in data, AI, and tech achieve twice the growth and up to 2.9 times the total return to shareholders of their peers.

Read the complete report by McKinsey & Company on Europe’s grocery retail market here.