By Moritz Felix Lück

Sellers rejoice, buyers suffer—the continued increase in sale prices for retail parks and hybrid malls in Germany is pushing demands on due diligence and the management of objects in this asset class ever higher. For investors, retail parks’ image has changed: Until a few years ago, they were a non-core product. Now, quality, well-located, and long-term-leased retail parks are considered part of the core segment.

This development increases the pressure to further professionalize the industry. The goal is to keep the risk-return ratio and the earnings situation at a constant level. An important approach to retaining or even increasing property values in times of declining returns is a 360° brand strategy.

Branding makes retail parks safer investments

Retail parks that are developed and managed as brands are more profitable than unbranded (no-name) centers. This is true with regard to investors and tenants alike. An analysis by GfK of more than 250 retail parks in Germany shows that retail parks that are developed as brands have lower risk profiles for investors. Basically, branded centers perform better than those that are not brands. That’s because “no-name centers” are extremely dependent on hypermarkets as anchor tenants because they have a low non-food share of tenants.

Branded centers are more diversified and reach an average productivity per unit of area that is 3% higher than non-branded centers—despite their much greater proportion of lower-turnover, non-food suppliers. In other words, branding strengthens retailers’ sales and lowers the risk for investors through diversification. Diversifying the tenant mix in branded centers also achieves higher rental income for investors. The significantly higher proportion of higher-margin, non-food vendors compared to unbranded centers allows this.

The great challenge for investors and operators is to provide branding and 360° brand management. There are widely divergent ideas about what is meant (or not) by this in the real estate industry. I present a holistic brand approach below, which establishes a systematic, structured, and customer- and market-oriented product policy as a basis for all asset and center management. This approach is based on brand instruments that are already common in the FMCG sector. Considered structurally, after all, retail parks are also products that need to be developed and managed with appropriate instruments.

Positioning, profile, and branding—creating added value to counter yield compression

Brands are a wonderful phenomenon—basically nothing more than an idea, yet enormously powerful. Brands make it possible to obtain a higher price for the same performance as would come from an unbranded provider because a brand positively and sustainably differentiates one product or service from another from the perspective of the relevant target groups.

To get started, we must first answer three simple questions.

- Question 1: Where am I?

- Question 2: Who am I?

- Question 3: How do you recognize me and my reliability?

Now, a fourth question: Can every investor and center operator answer these questions for each center?

Be honest with the answer, because it is about future viability. In times of increasing yield compression for investors, the answer to this question is crucial for ensuring returns. Proper strategic alignment and corresponding operational management are indispensable, especially for investors who invest only in core or core+ products.

Those who invest in value-add and opportunistic objects have the corresponding ability to (re-)orient a location. It is also of fundamental importance for retailers’ expansion managers to be able to understand a center’s quality.

Profiling

Establish a profile in all material respects. Profiling is aimed at delineation and core competencies. It means the detailed execution of the positioning of a precision-tailored product.

The aim is to make clear what consumers (and tenants) can find and expect on site. It is equally important, however, to define what a center does not provide. Hornbach is a very good example of the successful profiling of a big-box operator.

Centers without target-group and demand-oriented positioning (see Question 1 after “Positioning”), without a clear definition of what they stand for and what they don’t (see Question 2 after “Product concept and profile”), and without a narrowly-defined value proposition and integrated communication (see Question 3 after “The brand”) give investors problems.

From the merchants’ perspective, it is important that a retail park supports tenants in their own brand management. In addition, good retail parks ensure that tenants earn more revenue by coupling effects than they would at other sites. Next to generating customer loyalty, that is a retail park’s most important task as a brand. Sites with good track records are always attractive expansion targets, partly because of their higher productivity per unit of area.

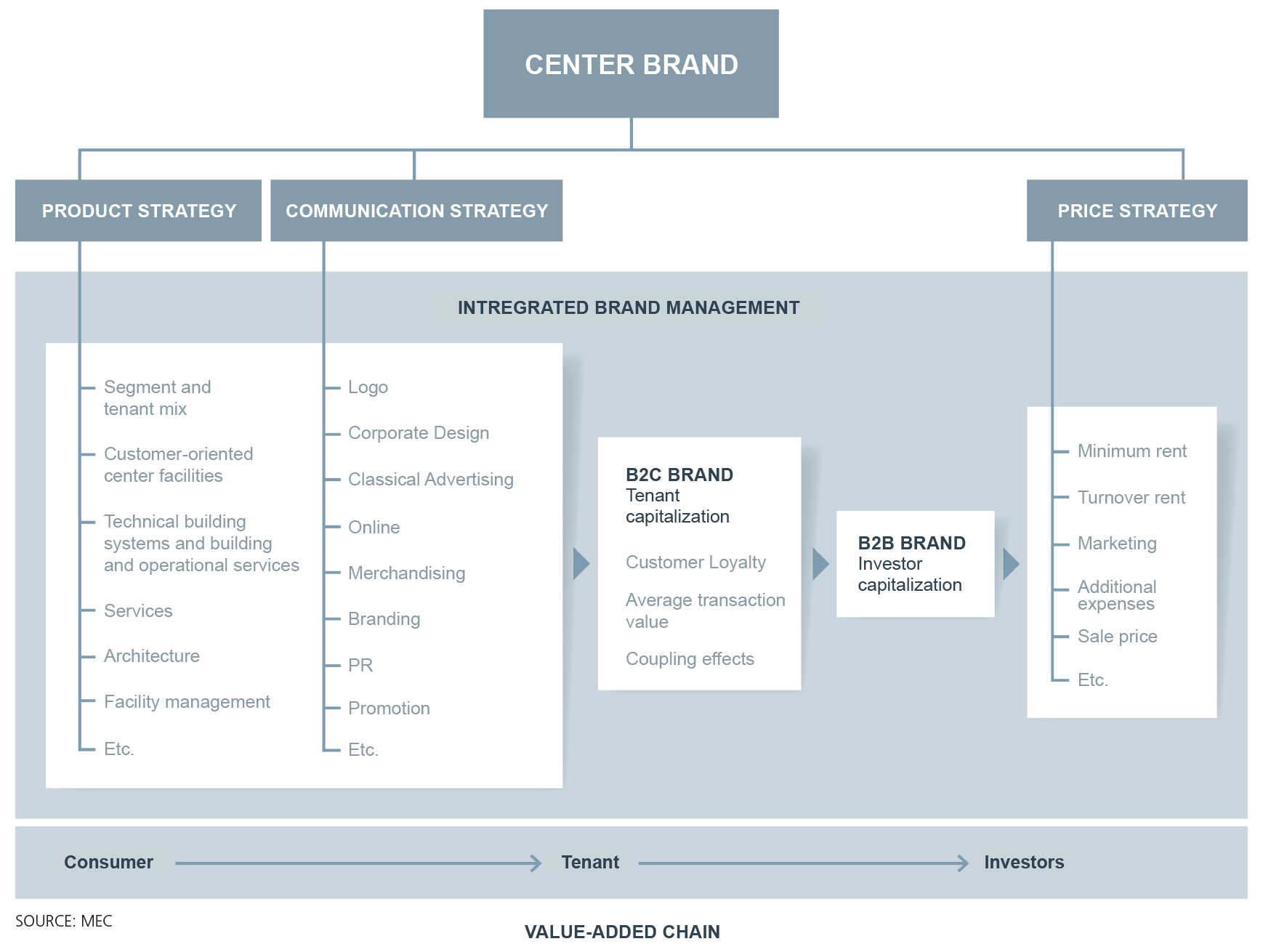

Retail parks are always inextricably intertwined B2C and B2B brands. This must be kept in mind, because tenants capitalize on the B2C aspects of center brands. Investors can only realize the added value in monetary terms that B2C center brands bring to tenants in the B2B context, however.

A strong B2C brand enables investors to set the higher prices garnered by branded products, for example with regard to rents and sales.

Only with a B2B brand does a branded park become effective from the investment side (see graphic “Center brand”). Established center brands are an expression of the quality and stability of a retail park when the brand is well managed.

The primary target group for a center brand is the consumers, who appreciate brands for many reasons (see “Defining target groups”). They prefer shopping centers with clear and consistent product and service promises. With retail parks, it’s all about fast, efficient, and time-saving shopping. They must be easily reached by car, have free parking, and have good retailers and services all under one roof with a reasonable quality of stay.

Interdisciplinary product design as a brand basis

The same applies for the real estate industry: When it comes to branding, product policy and product management are key issues! Structurally, retail parks are products like any other. They are complex products, however, that also have to satisfy the requirements of B2B and B2C activities.

The center’s product and performance characteristics must be defined based on an analysis of the target groups and competition. This covers elements such as the segment and tenant mix, center facilities, the building’s technical equipment and operating technology, branding, signposting systems, and more. These aspects alone show that a 360° brand strategy is a very complex undertaking, requiring the very close cooperation of various stakeholders, including investors, operators, service partners, retailers, and architects.

Such cooperation is impossible without a coordinated and comprehensive product concept that views the center product from the perspective of service provision rather than that of segments. Overcoming disciplinary boundaries to favor a task-based analysis is a core challenge for the real estate industry.

Good product design should, if possible, also create a real USP inherent in the product. Such an in-depth analysis of a retail park’s relevant competition is necessary to identify a demand-oriented USP appropriate to the audience. The important thing is to be guided by your audiences’ needs.

A USP inherent in the product could be, in addition to the tenant and segment mix (rather difficult), services, modern design, new store concepts, etc. A multidimensional USP is ideal, for example composed of a good tenant mix, pleasant shopping environment, and good services.

Tenants inhabit a dual role in a shopping center’s product concept. They are service providers in the B2C context and fulfill the brand promise of the entire retail park (for the consumer target group). In the B2B context, they are paying customers (for the investor and the operator) whose wishes must be taken into account.

Tenants’ requirements must therefore be considered in all aspects of the brand and value proposition, including with regard to the product concept. There is already acute need for this, for example with regard to the flexibility to respond to the changing area needs of tenants from different segments. Drugstores and hardware stores, for example, are tending to grow, while hypermarkets and electronics stores are likely to reduce their areas.

When space is freed up, this provides opportunities to alter a center’s segment and tenant mix. This is important in order to achieve higher frequency and coupling effects with a strong center brand. The adjustments also help in continuing to provide clear and competitive positioning.

Positioning

A fixed place in the competitive landscape of customers’ demand maps: Positioning means setting up a center to serve clearly-defined target groups and their needs as a retail location. A demand-orientation can be established only when a center differentiates itself from the competition and/or closes gaps in the required coverage for consumers. Matching one-to-one what the competition provides creates no clear positioning.

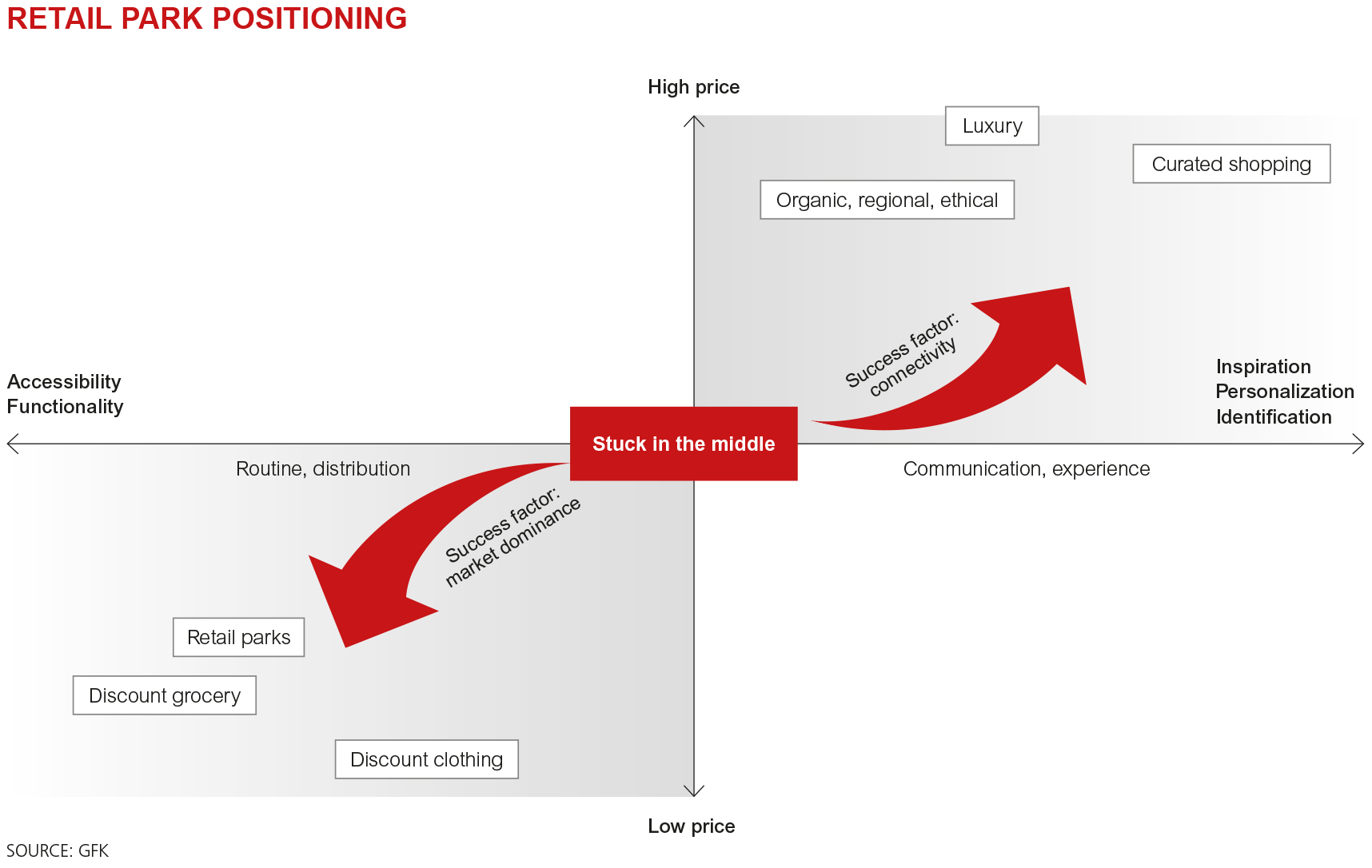

The graphic below shows how the retail park commercial format is generally positioned from a consumer perspective:

A look at the four-quadrant matrix shows how important the positioning of retail formats is. The coordinate system consists of price orientation on the Y-axis and purchase motivation (routine shopping versus experience shopping) on the X-axis.

The very center is highly problematic. That is the dangerous market position that has no particular profile and has been losing market share for years. For retailers and retail properties, there are basically only two ways to move away from the gray and deadly middle: routine or experience shopping.

Shopping centers and their tenants are evolving towards experience shopping. Shops and centers are taking on communicative functions. Progressive concepts achieve this with a multichannel strategy, since consumers expect high connectivity with other areas of life.

When targeting price-oriented routine shopping, stores and the retail park platforms have a clear distribution function. To be successful in this sector requires a market-dominant position, as the sales volume must be large due to the low margins.

Successful branded retail parks are clearly positioned in the “price-oriented with little experience” quadrant. Many typical tenants in retail parks have also been working on their positioning in recent years.

Segments such as the food trade, drugstores, and hardware stores have lifted branding, marketing concepts, shopfitting, and advertising to a new level. Other segments are not so far along.

Integrated brand management is a daily task

The product concept must be developed continuously because the demands of consumers and tenants are constantly changing. This must be accounted for through anticipatory further development, for example of the leasing concept and quality of stay. After all, brands are the result of a variety of integrated measures, and customer experiences based on them, carried out over a longer period.

Brand management is the concerted and interdisciplinary planning, orchestrating, transferring, and monitoring of these measures.

An essential factor that causes the failure of 360° brand management is a lack of true interdisciplinary work. A strong brand cannot be established if the center management, rental management, marketing, and technical and commercial property management do not manage a retail park as a brand in the same team and instead each work more for themselves and according to their own logic. How is this implemented in daily operations?

The center management is a brand’s main maintainer and developer. The local staff take care of marketing and PR, provide services to tenants, initiate measures to promote sales, ensure good quality of stay, etc. They also ensure that service partners like facility management providers fulfill their duties to the center. A clean building, rapidly cleared snow, and many other things are visible expressions of whether a center is a positive brand.

Furthermore, the center management must take care of strategic issues. A brand-appropriate rental concept must be developed and implemented in collaboration with the rental management. An active and prudent center management on-site can detect risks and opportunities for product and brand early.

This knowledge may allow it in time to develop appropriate measures in close cooperation with other disciplines—whether it’s to prevent trading down or to take advantage of opportunities to increase value. The target consumer groups are the start and end point for these considerations, too.

Retail parks and all other retail buildings must be geared to the needs of their customers. Few would disagree with this statement. The question is, how does one define target groups or, more precisely: How should we define target groups now to create a retail property as a (brand) product?

A small test will help here: Whom does the following audience definition apply to?

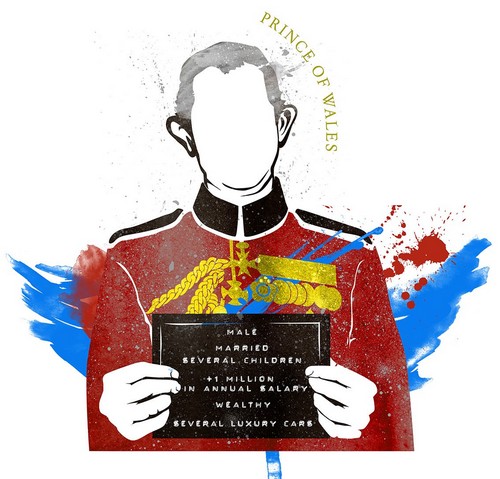

Same data, but certainly not the same target audience. This simple example shows that socio-demographic data alone are simply insufficient for accurately defining target groups.

Those who want to develop a shopping center must decide whether they wish to attract customers like Prince Charles or Ozzy Osbourne.

If one chooses Ozzy, the hedonist, they can, however, address other hedonists as well, regardless of age or origin.

That’s because the lives of Ozzy and the hedonists have much in common, even as Ozzy and Prince Charles do not—even if they are sociodemographic twins.

Connecting with the lives of the target groups is essential for survival. Many products, including retail parks, have no real, product-inherent USP.

The following is an example from the consumer goods sector: Whether you have a smartphone from Apple or Samsung basically doesn’t matter as far as its benefits are concerned (battery life excluded).

What’s more important from a consumer perspective is which manufacturer and which model best fits their self-image and their lives. The heavy competitive pressure requires that providers make an emotional case to consumers and connect with their respective living environments.

This competitive pressure and the expansion of retai, has also shifted the market power of retail outlets in favor of consumers. It is important to look at the people and the entire frame of reference of their living environments. This is the only way to realize that Ozzy and the hedonists belong to the same target audience.

Rock star or rye toast—simple guiding questions for brand due diligence

Whoever acquires an object as an investor should carry out brand due diligence. The cooperation between the fund, asset, and center managers necessary to identify and acquire a target object can allow the investors’ provisos and expected returns to be checked more sustainably for success.

It is necessary to consider whether the product, target audiences, and competitive position match, whether a brand is present, whether it has been maintained, etc. A formally strong tenant mix alone is not meaningful enough to be sure one is buying a good product. Such brand due diligence is also recommended for tenants moving to a new location. It serves the same purpose of minimizing the risks associated with expansion.

The usual checks such as profitability and the condition of the building and its equipment help, but they leave aside many aspects that are important for a retail park’s continued success. Be honest: Who so far has been in the habit of comparing a center’s offer with the catchment area’s requirements? Buyers are often enough satisfied with the fact that the tenant mix is composed mostly of well-known chain stores.

The main focus is on leases, maturities, etc. Such a narrow focus can miss the fact that a nominally strong tenant mix may already no longer cover the demand from consumers and the competition. An erosion of demand coverage occurs only gradually, but it can be caught in time through a thorough examination.

Brand due diligence is a comprehensive examination of a retail park from the perspective of consumers, tenants, and operators and is recommended for locations above a certain size.

Before buying a retail park or big box-oriented shopping center, it is especially important to perform an expert audit of brand-related aspects to determine whether a commercial location really has a future as an overall concept. Such an audit is complex and requires adequate expertise, data, and analysis.

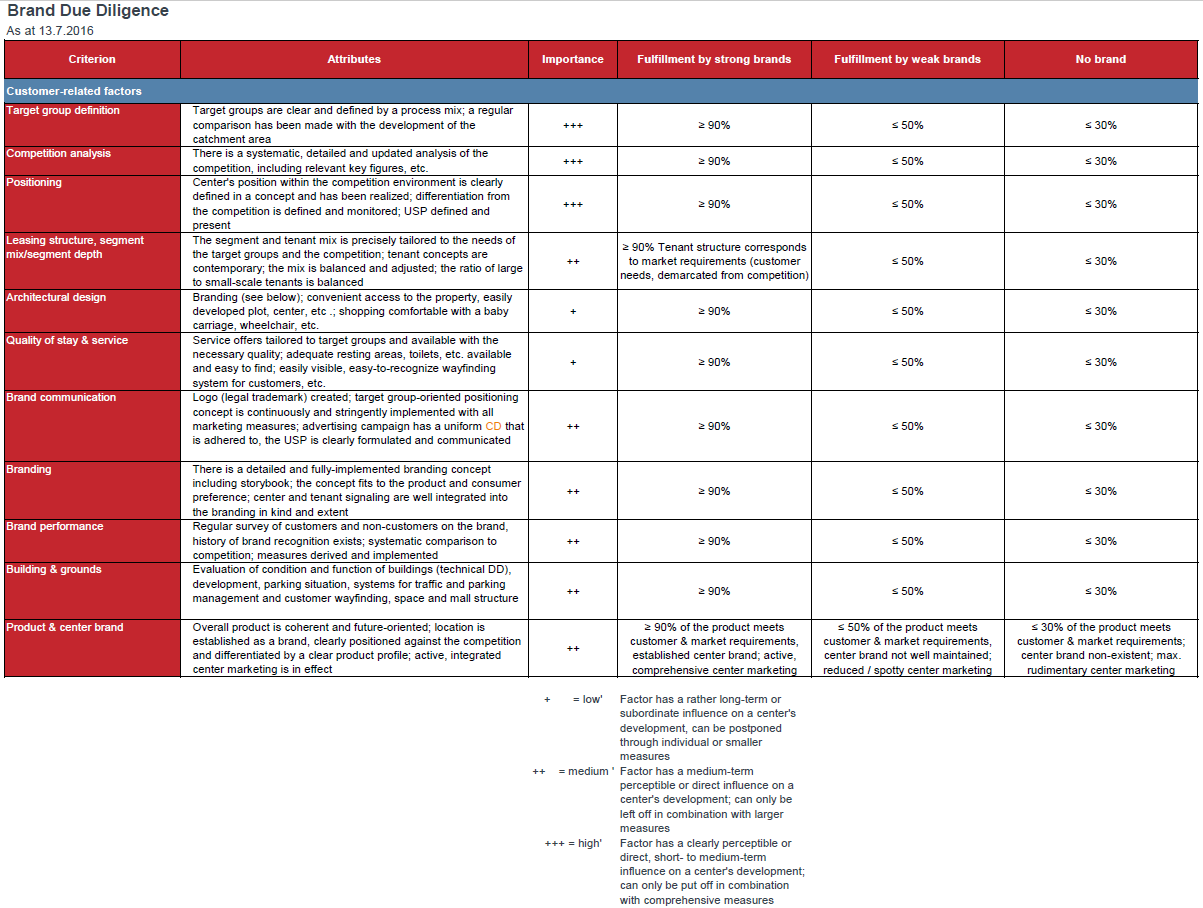

The following table shows the general key questions and themes for brand due diligence alone that must be explored and evaluated in relation to the consumer. The aspects relating to tenant requirements are excluded.

Brand due diligence regarding customer needs is based, like all customer-oriented approaches, on precise knowledge of a respective center’s customers and the target groups in the catchment area you want to reach.

Of equal importance is whether there is a detailed analysis of the competition that clarifies, among other things, the intersections of one’s own position with that of each of one’s competitors. The intersections include, for example, target groups, the offer (segment and tenant mix), and modernization intervals.

Only after comparing them with the competition can one determine whether a center has an elaborate positioning concept, i.e. whether it covers a clear need and has a decisive and sustainable unique selling point that the competition lacks.

The entire retail park product must be examined in this regard. Criteria for this are, for example, the segment and tenant mix, the modernity of tenant concepts, the center’s technical equipment, branding, and quality of stay. Based on what is hopefully a good product, a corresponding communication of the brand should be carried out that implements and transmits the positioning and brand promise. One must also consider at this juncture whether adequate marketing budgets are available. Branding is impossible without communication.

Pointedly: Without careful brand due diligence, the decision to buy a retail park or a big box-oriented shopping center is a gamble. Whoever wants to be really sure in the end that they’re adding a rock star and not rye toast to their portfolio must not skip this crucial test.

Conclusion: A 360° brand strategy is a long-term success factor for asset management

E-commerce is leading parts of retailing to decouple from the retail real estate market: Online sales tend to need fewer retail properties, even with sometimes high click & collect rates of up to 40%. Due to various factors, one can assume that shopping in the food retail segment and others in local supply will continue to take place primarily offline in the coming years. This makes retail properties that are heavily oriented toward local supply more interesting for investors. This absolutely includes retail parks, which are less susceptible to the effects of e-commerce. But the number of objects in Germany is limited and good retail parks are now also being sold at 20 times their purchase price.

Since the starting point for institutional investors is becoming increasingly similar due to historically low financing costs and because, at least in the traditional core segment (without retail parks), investors have very similar return expectations, properties can be valued and priced sustainably and successfully only by identifying a property’s long-term success factors. A 360° brand strategy is a long-term success factor.

The brand, based on a target group and competitive product concept, is the foundation for every managed retail property. It is therefore crucial that retail parks, too, are a distinctive and credible brand. Asset and center managers must actively build that brand. To communicate the brand effectively to the customers, it is almost imperative to form an advertising community among the tenants and the center management. Tenants and operators then jointly ensure that the center develops positive brand recognition—ideally one that is better than its competitors.

If asset and center managers use the brand to position the retail park successfully in the market, they can attain a dominant market position in the object’s catchment area and a high level of acceptance and strong customer loyalty. This is absolutely necessary for the format’s fundamentally routine-oriented shopping positioning. The dominant market position allows tenants to achieve high productivity per unit of area, which puts them in a position to change their concepts and constantly to offer their customers something new. The aim is a long life cycle that ensures sustainable returns and rising value.