In the UK, 15 percent of respondents rate their situation as better than in the previous year, while 40 percent rate it as worse. In Italy, only 8 percent of respondents rated their economic situation as better than in the previous year, while 30 percent were convinced that it had worsened. Respondents from countries outside Europe, on the other hand, were much more optimistic. 26 percent of US citizens consider their economic situation to be better than in the previous year. In China and India, the figures are as high as 50 percent and 58 percent respectively.

But what factors are responsible for the negative assessment of European consumers? More than one in three (37 percent) is worried about rising food prices. For one in four (25 percent), rising energy prices are a cause for concern. The first two rankings have not changed compared to the previous year. Europeans worry about global conflicts and the escalation of crises. 18 percent of all respondents are concerned about wars, political instability and the development of the party landscape in Europe.

These factors are also having an impact on consumers’ propensity to spend. Although the consumer confidence index in Germany rose compared to the average of recent years up to April 2024, it is still below the long-term average. Consumer confidence is particularly negative in many South-Eastern European countries such as Greece, Slovenia,

Hungary, Cyprus and Turkey, but also in Estonia. European consumers are reacting differently to the rising prices. Consumer surveys by NIQ show that 93 percent of consumers have changed their shopping behavior and adjusted their spending habits. Which adjustment strategies consumers pursue varies greatly from country to country.

On average, however, each consumer pursues four of these savings measures:

- 40 percent: purchase of brands on offer

- 33 percent: switch to cheaper offers

- 33 percent: pay attention to the costs of the entire purchase

- 33 percent: more frequent shopping at discounters

- 31 percent: purchase of private labels

- 29 percent: stock up when their preferred brand is on offer

In Germany, the main strategy is to buy brands on offer. However, many consumers also switch to private labels or shop more frequently at discounters. A comparison of the discounters’ market shares in 2019 and 2023 – i.e. before and after COVID-19 – shows an almost identical market share of around 40.5 percent. In the first year of the pandemic, however, the market share fell significantly to 38.7 percent. This can be attributed to consumers’ focus on food. As inflation picked up, discounters were able to regain ground and increase their market share to pre-crisis levels.

In Spain, France and Italy, people tend to look at the total amount in their shopping baskets rather than buying from discounters. In Spain and France, the share of discount stores stagnated at 10 percent and 12 percent respectively. Despite average inflation rates of 5.8 percent in 2023 and an expected 5.5 percent in 2024, very strong growth in discount stores was observed in Norway. Their share of FMCG turnover rose from 67 percent in 2019 to 72.5 percent in 2023. This is due to the very high overall price level for food in Norway, from which the discounters Kiwi and REMA1000 were able to benefit.

Consumers in Hungary, on the other hand, were reluctant to switch to discounters. The country’s discounters, including the three most strongly represented chains Lidl, Penny and Aldi, were able to increase their share of the FMCG business from 26.7 percent in 2019 to 29.3 percent in 2023.

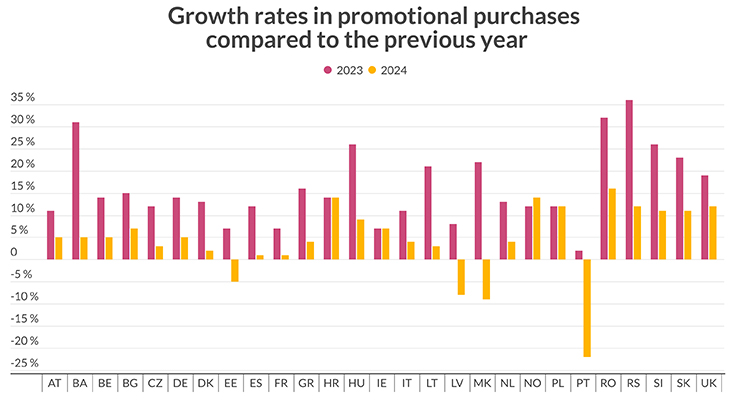

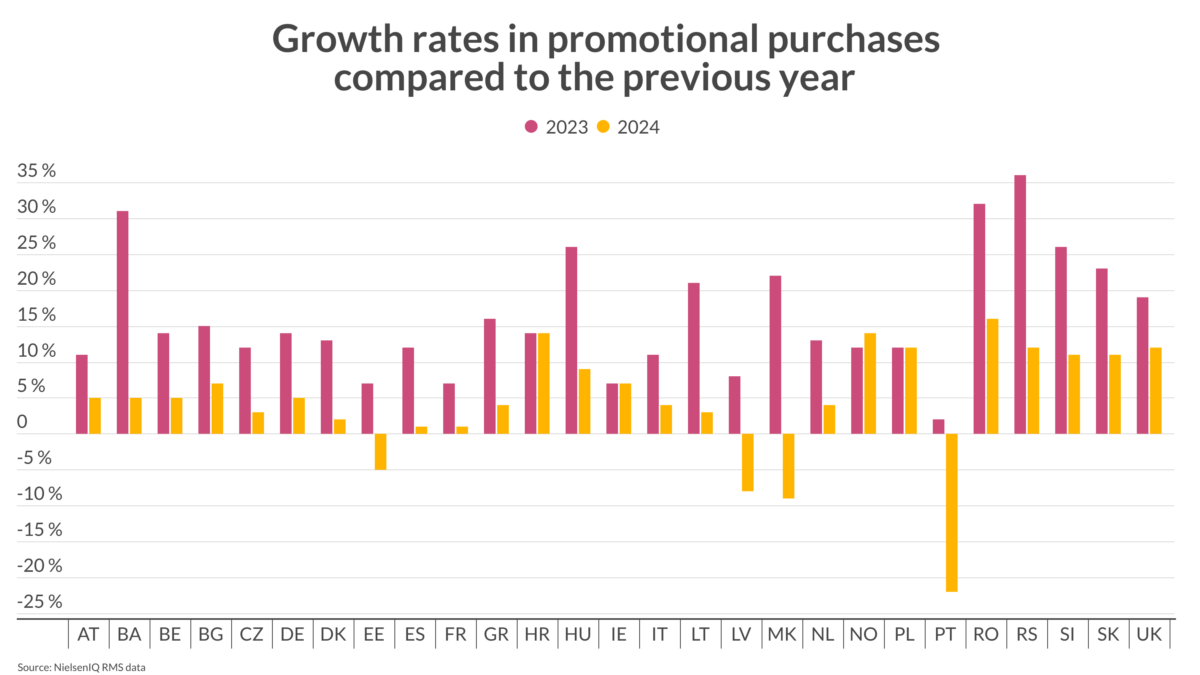

At European level, the use of promotions is very widespread. During the peak phase of inflation, the proportion of FMCG items purchased on offer increased in almost all countries. The highest increases from 2022 to 2023 were recorded in Eastern European countries such as Serbia, Romania, Hungary as well as Bosnia and Herzegovina, which also recorded the highest price increases and the highest spending shares for FMCG in total purchasing power. In Romania, prices for FMCG products rose by 16 percent. At the same time, the proportion of household spending on FMCG was already at the European top at 27 percent, so there was little scope for further budget increases.

In Western Europe, Germany recorded the strongest growth in promotional purchases with an increase of 14 percent. In contrast, the overall share is rather low at 25 percent and is significantly higher in the UK at 33 percent and in Austria at 37 percent. A breakdown of FMCG purchases by product group shows that alcoholic beverages are preferably purchased on offer. In the Czech Republic, they make up a share of 72 percent. The lowest proportion of promotional purchases is recorded in healthcare products. The urgency of the need for these products and strong product loyalty certainly play a decisive role here.

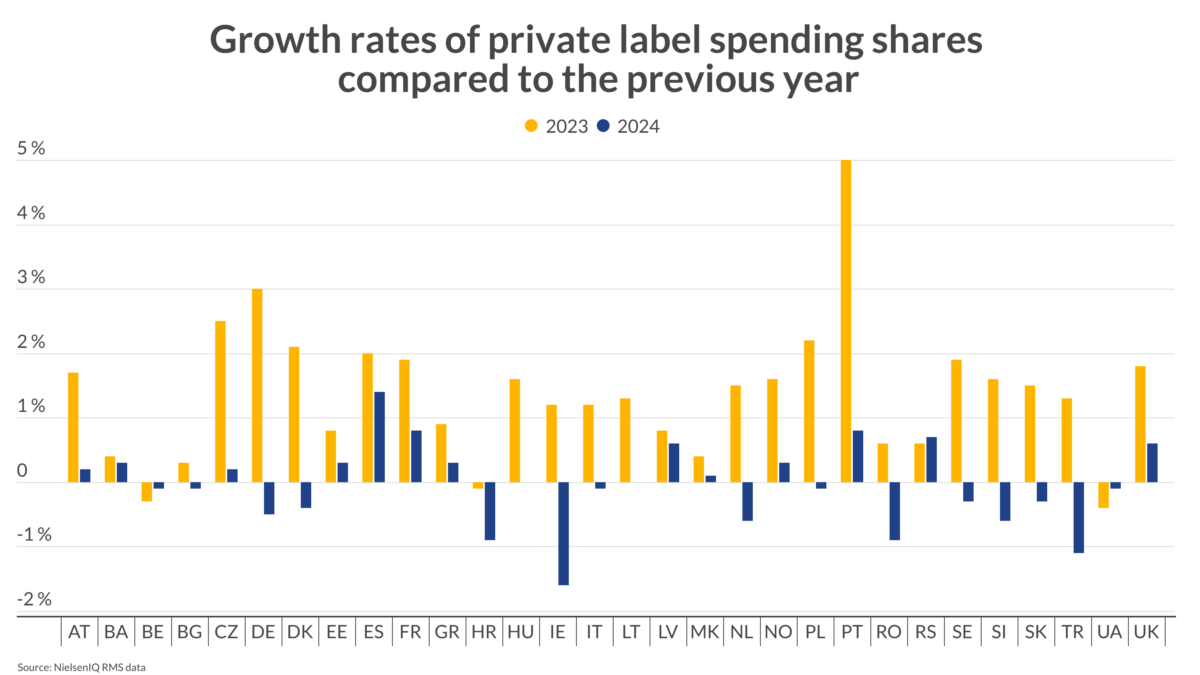

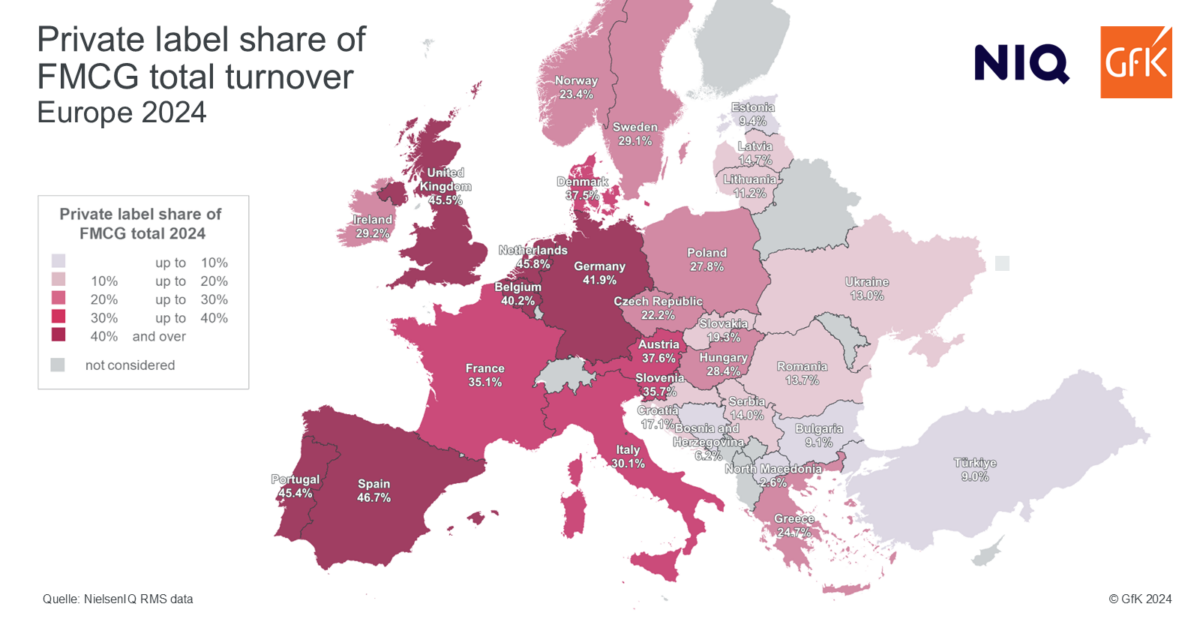

In contrast, the purchase of private labels is more widespread in countries with higher purchasing power than in Eastern European countries. Countries such as Spain, the Netherlands, the United Kingdom and Germany have a share of private label FMCG purchases of just under 42 percent. Spain leads this statistic with a share of 47 percent. Private labels generally do not differ in quality from manufacturer brands, but are often significantly below the price level of the major and established brands.

At the other end of the European scale are countries such as Turkey, Bosnia and Herzegovina as well as Bulgaria. There, the share of private labels is less than 10 percent. The ability to buy fresh produce more cheaply at the farmers’ market is certainly a decisive factor in countering price increases.

In 2023, growth in private label and supply purchases was observed in almost all European countries compared to the previous year. However, as inflation rates flatten out, this trend is losing momentum or even declining in the current year. At -1.6 percent, the sharpest decline in private label purchases was recorded in Ireland, where growth of 1.2 percent was measured in the previous year. In Germany, the previous year’s growth of 3 percent could not be repeated. Instead, a decline in private label purchases of -0.5 percent was recorded.

After 2023 was characterized by an adjustment to the increased cost of living, the economic uncertainty remains in 2024. However, the first signs of rising consumer sentiment are slowly becoming apparent. The share of purchases on offer remains constant in 2024 and NIQ was able to measure growth in FMCG sales by unit for a quarter of European markets in the first quarter of 2024. This means that, after a long phase of price-driven growth, more products are being purchased again and consumers are more optimistic about the future.

About the study: NIQ-GfK analyzed purchasing power, retail turnover and the retail share of consumers’ total expenditures for 2023 as well as consumer price trends 2023 and 2024 in Europe. This year, a special chapter sheds light on the fears and adaptation strategies of European consumers. In doing so, the study offers a valuable point of reference for retailers, investors and project developers.