Even though the gas shortage feared last year did not materialize during the winter and energy prices have leveled off somewhat at present, the energy situation, inflation, and supply bottlenecks continue to cause uncertainty within the economy and among retailers and consumers.

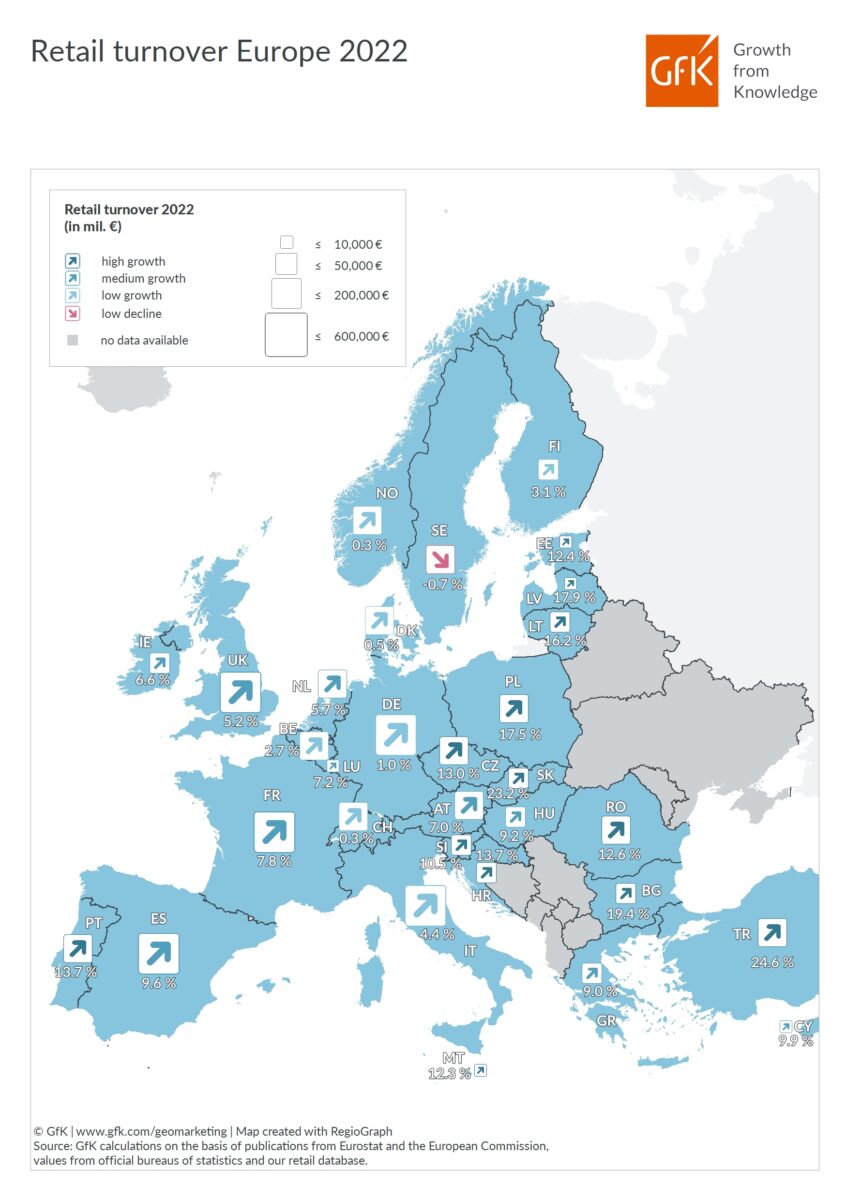

Due to significantly higher prices resulting from these crises, the retail sector in the 27 EU countries was able to significantly increase its turnover again in 2022. Last year, around 2.83 trillion euros flowed into the retail sector, representing a 6.5 percent increase in turnover. The highest gains were recorded by the Eastern European countries, all of which had growth rates of over 9 percent, with Slovakia taking the clear first place at 23 percent. This is shown by the new study on retail in Europe, in which GfK examines important key indicators.

While retail turnover in Eastern Europe increased significantly in 2022, the situation was different in Scandinavia: Finland, for example, recorded a turnover increase of only 3 percent, while in Sweden retail turnover actually declined slightly by 1 percent. A more detailed look at fast-moving consumer goods (FMCG) shows a similar picture for Eastern European countries – with Slovakia occupying the top rank. Across the EU, the growth rate of daily consumer products was 6.9 percent, while in Slovakia turnover for food grew by as much as 38 percent – more than twice the growth for nonfood sales.

In addition to retail turnover, the study analyzes the distribution of purchasing power in Europe as well as the retail share of consumers’ total expenditures and consumer price trends in 2022 and 2023. Special chapters take a closer look at the development of inflation by purchasing power product lines and the situation in the retail trade for electrical household appliances and consumer electronics.

Additional key results at a glance

Purchasing power: Following almost unchanged purchasing power in 2020 compared with the previous year and moderate purchasing power growth of 3.9 percent in 2021, net disposable income in the European Union rose at a much faster rate in 2022. Across the EU, the average per capita purchasing power was 18,468 euros, which represents a nominal growth of 6.1 percent.

Share of retail turnover in private consumption: Although retail turnover grew significantly in 2022, the retail share of private consumer spending recorded a decline for the first time in years. Even though the desire for shopping returned, as did more tourists, retail consumption in 2022 was suppressed primarily by high inflation rates as well as high energy prices. Accordingly, the retail sector’s share of private consumer spending declined by 4.6 percent to 34.2 percent in the 27 EU countries, when compared to 2021. Hungary, a country particularly affected by inflation and rising prices, had the largest retail share of consumption at 49 percent, followed by Bulgaria and Croatia at 47 percent each.

Inflation: After inflation in the 27 EU countries reached a record level of 9.2 percent in 2022, it is forecasted to drop to 6.7 percent in 2023. This, however, will be offset since wages in the countries of the European Union are expected to rise by 5.9 percent in 2023. Nevertheless, this will still not fully compensate for the loss of purchasing power due to inflation. Prices will rise particularly strongly in Hungary at 16.4 percent, but double-digit growth in consumer prices is also expected in the Czech Republic, Poland, and Slovakia.

Development of inflation by purchasing power product lines: Consumers in regions with low purchasing power have to save a larger share of their budget for FMCG. While the Swiss special measures of import taxes led to a very moderate price increase of 4.1 percent for FMCG, consumers in Romania and Hungary had to cope with price increases as high as 22.8 percent and 37.8 percent, respectively (January 2022 to April 2023).

Situation of tech retail: The European market for technical consumer goods recorded a 1 percent decline in sales in 2022. At the same time, promotions and key annual shopping events reached a new record high. In the first quarter of 2023, there was a decline in sales of entry brands (down 9 percent) and in the mid-priced standard segment (down 3 percent) compared with the first quarter of 2022, while sales of premium brands increased slightly despite the crisis – particularly in some Eastern European countries.

You can download the GfK study here: