- Attractiveness Index for 15 European countries reaches three-year high

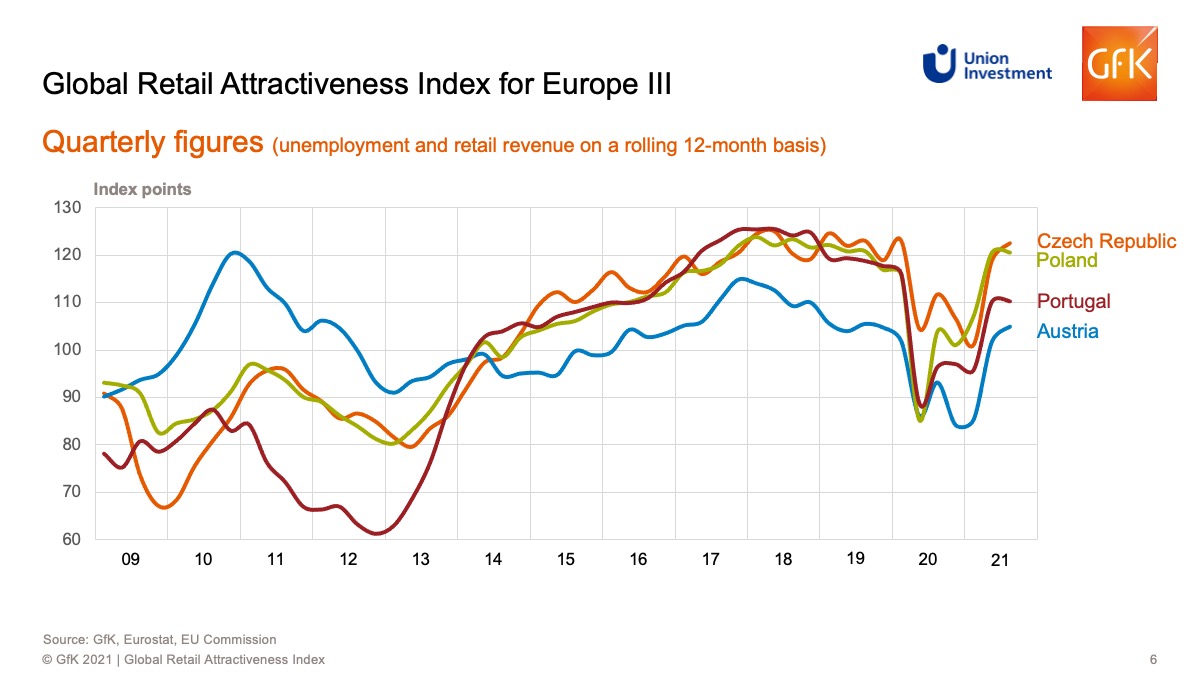

- Germany, Czech Republic and Poland are new top trio in index

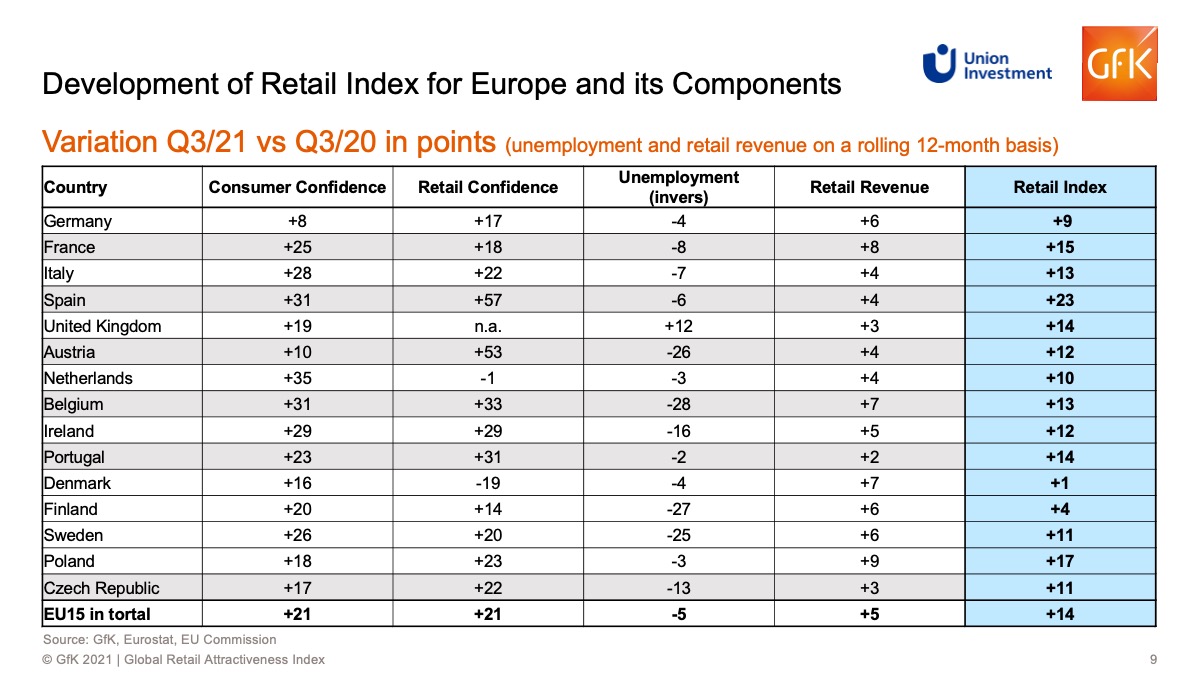

- Sharpest rise in Spain

European retail markets turned the corner in the third quarter of 2021. The Retail Attractiveness Index, which is compiled jointly by Union Investment and GfK and measures the attractiveness of the 15 most important retail markets in Europe, recovered significantly in the second and third quarters of 2021, climbing to 113 points. That figure is 14 points above the prior-year period and represents a three-year high for the retail index in Europe. The previous peak was 115 points, recorded in the third quarter of 2018. By the second quarter of 2020, the retail index had fallen to 89 points, its lowest level to date. It then flatlined at a below-average level up to and including the first quarter of 2021. A figure above 100 points indicates an above-average reading.

“The strong increase now measured shows that we’ve left the challenging lockdown times behind us, and that both consumers and retailers now have a much more positive outlook,” said Olaf Janßen, head of Real Estate Research at Union Investment.

Returning optimism is reflected in the index’s two sentiment readings. Consumer sentiment and retail sentiment both increased by 21 points over the course of the year, taking them back into above-average territory at 109 and 110 points, respectively. The labor market continued to be a source of major support in the third quarter (120 points; minus five points), as did retail sales (117 points; plus five points).

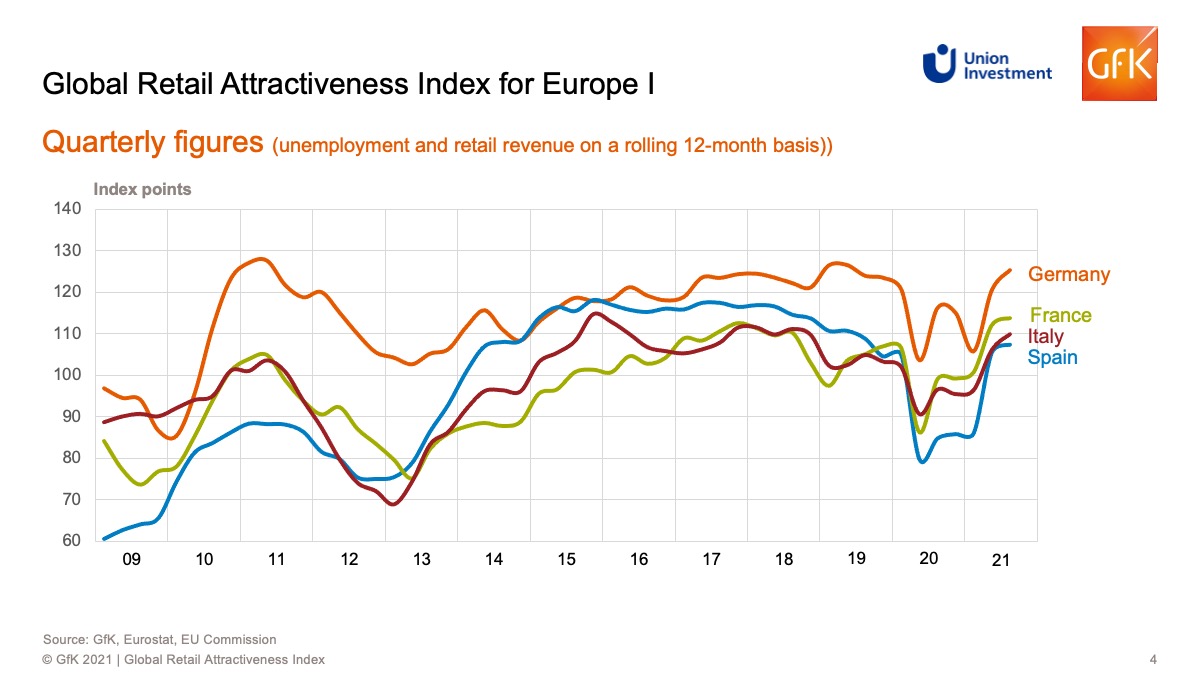

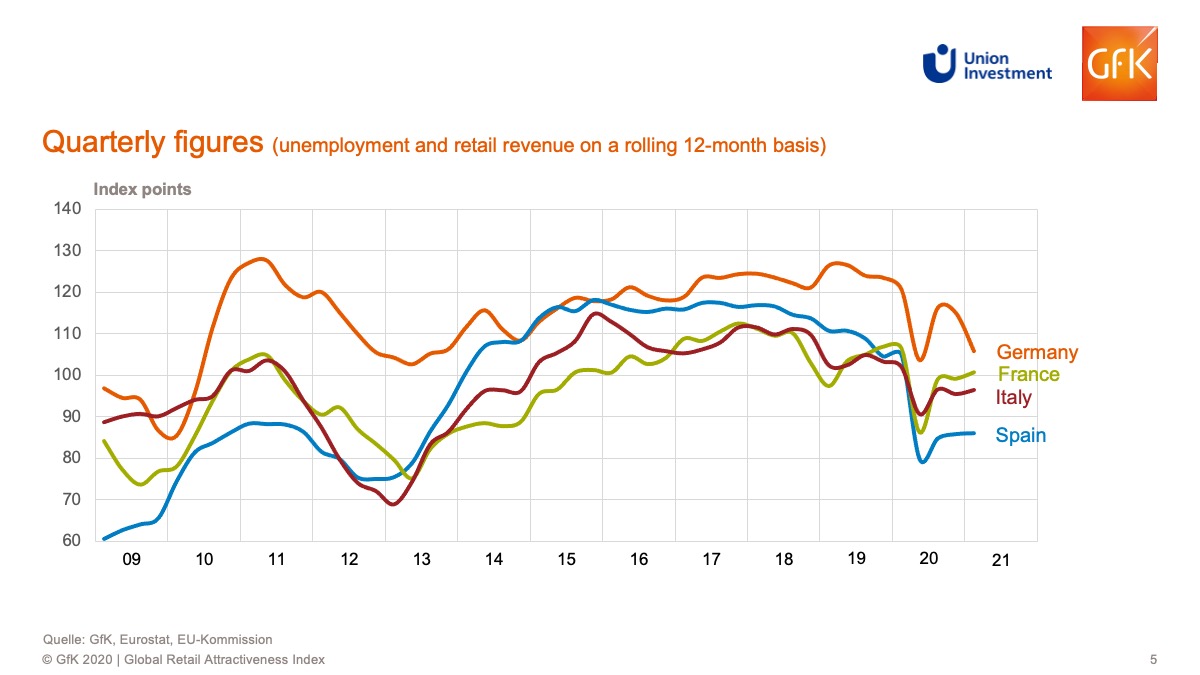

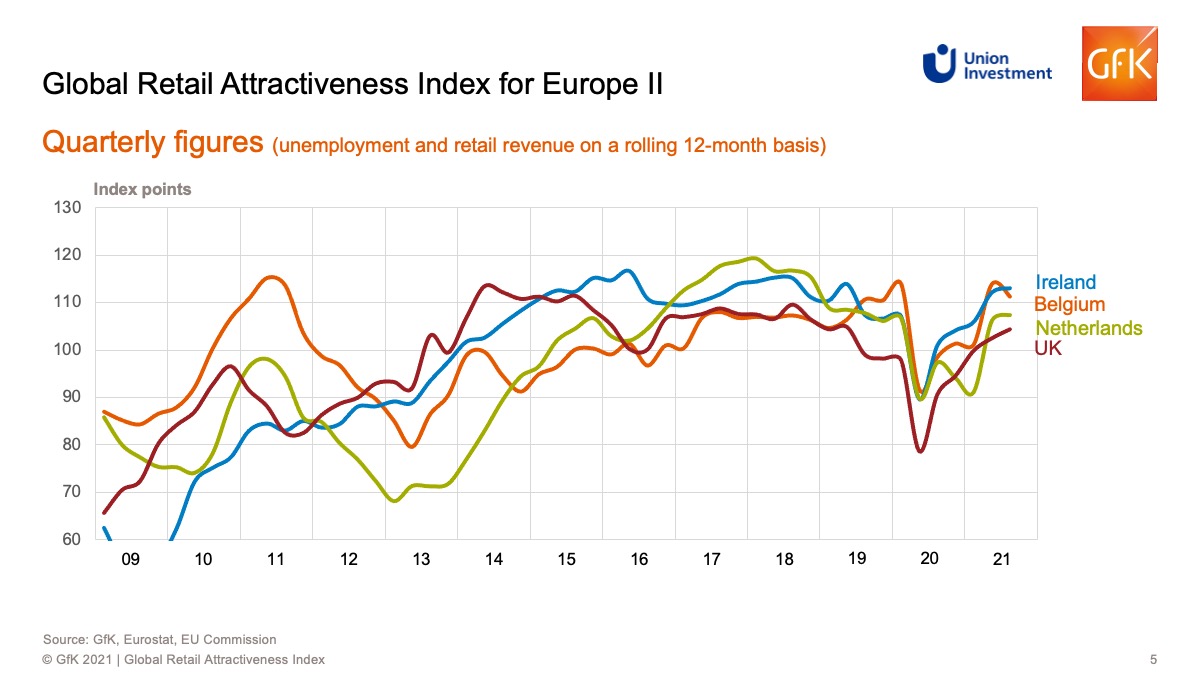

Compared to the third quarter of 2020, the index strengthened across all 15 European countries covered. “The changes are mostly in the double-digit range, highlighting the vigorous recovery that is now under way,” said Janßen. The strongest rises over the year were posted in Spain (up 23 points), Poland (up 17), France (up 15), Portugal and the UK (both up 14). At country level, Germany regained its top spot with 125 points (up nine points), followed by the Czech Republic (123 points) and Poland (121 points). France occupied fourth place with 114 points. Sweden is currently the worst performer, on 98 points, being outstripped by the UK (104 points) and Denmark (102 points).

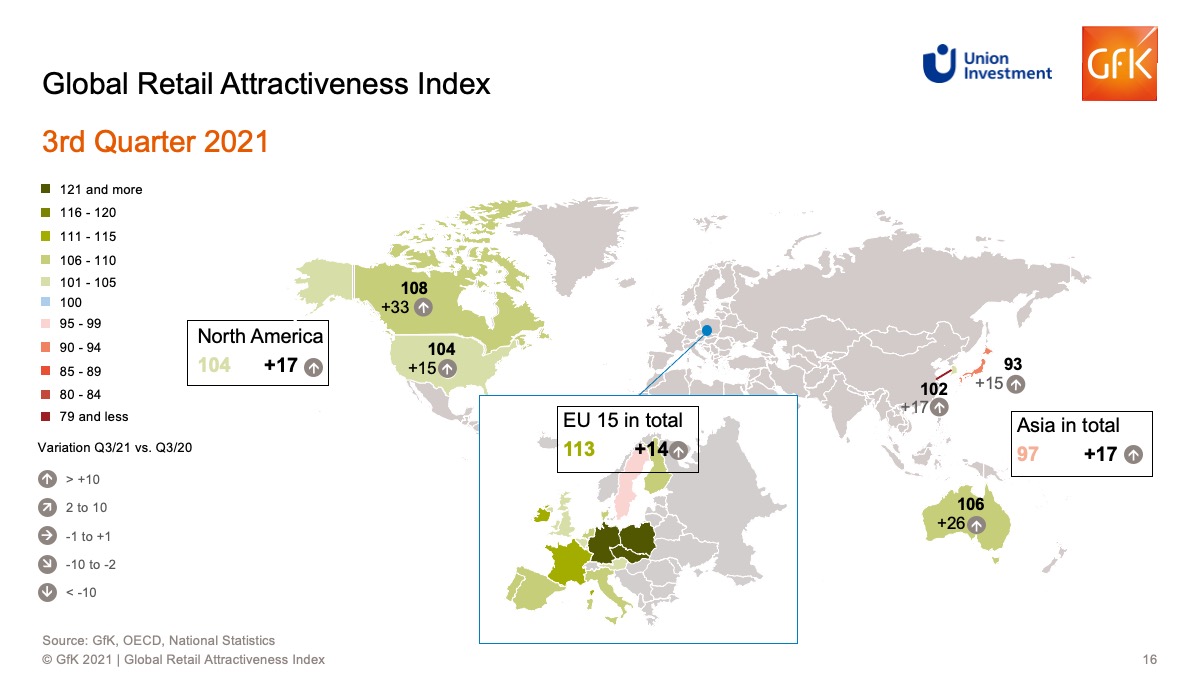

Like the European retail index, the global retail index also reveals encouraging developments in the markets under review. Both North America and the Asia-Pacific region were digging their way out of the crisis in the third quarter. The retail index for the North America region climbed to 104 points, while Asia-Pacific is still slightly below average at 97. Each of these regions gained 17 points, thus slightly outperforming Europe over the course of the year. The retail index for Europe nevertheless remains ahead of the two other regional indices in absolute terms.

All five of the overseas markets under review contributed to the sharp rise in the global retail index. That applies in particular to Canada, which added 33 points and delivered the strongest performance across all the markets covered worldwide. It now holds the top slot among overseas markets at 108 points. Canada is followed by Australia (106 points; up 26), the US (104 points; up 15) and Korea (102 points; up 17). As in the first quarter of 2021, Japan continues to bring up the rear at 93 points in both the global retail index and the overall ranking, despite seeing a strong increase of 15 points.

Key Facts

Europe emerges from the crisis in the third quarter. The Retail Index for Europe (EU 15) recovers noticeably in the second and third quarters of 2021, climbing to 113 points. This is 14 points higher than in the corresponding period of the previous year. This is the highest value in three years. In the third quarter of 2018, 115 points were measured.

This sharp rise is primarily attributable to sentiment indicators. Both consumer sentiment (109 points) and retail sentiment (110 points) increased by 21 points in the course of the year. The labor market (120 points, -5) and retail sales (117 points, +5) also continue to provide significant support due to their above-average levels.

In terms of the level of the Retail Index, Germany currently leads the field at country level with 125 points, followed by the Czech Republic (123 points) and Poland (121 points). France takes fourth place in the third quarter of 2021 with 114 points. At the other end, Sweden currently brings up the rear with 98 points, followed by the UK with 104 points and Denmark (102 points).

The encouraging news is that, compared with the corresponding period of the previous year, all the countries considered are up. The strongest gains were recorded by Spain with an increase of 23 points, Poland with plus 17 points, and France(+15 points). They are followed by the UK and Portugal, each with an increase of 14 points.

The weakest year-on-year increases in the third quarter were recorded in Denmark (+1 point) and Finland (+4 points).

Methodology

Union Investment’s Global Retail Attractiveness Index (GRAI) measures the attractiveness of retail markets across a total of 20 countries in Europe, North America and the Asia-Pacific region. An index value of 100 points represents average performance. The Europe index combines the indexes for the following 15 countries, weighted according to their respective population size: Denmark, Finland, Germany, France, Italy, Spain, Sweden, the United Kingdom, Austria, the Netherlands, Belgium, Ireland, Portugal, Poland and the Czech Republic. The North America index comprises the US and Canada, while the Asia-Pacific index covers Japan, South Korea and Australia.

Compiled every six months by market research company GfK, the Global Retail Attractiveness Index consists of two sentiment indicators and two data-based indicators. All four factors are weighted equally in the index, at 25 per cent each. The index reflects consumer confidence as well as business retail confidence. As quantitative input factors, the GRAI incorporates changes in the unemployment rate and retail sales performance (rolling 12 months). After standardization and transformation, each input factor has an average value of 100 points and a possible value range of 0 to 200 points. The index is based on the latest data from GfK, the European Commission, the OECD, Trading Economics, Eurostat and the respective national statistical offices. The changes indicated refer to the corresponding prior-year period (Q3 2020).