By Moritz Felix Lück and Manuel Jahn

The augurs of the beautiful, new trade epoch proclaim that the brick-and-mortar trade will disappear—and with it, commercial real estate. Dead malls in the US are used as evidence. The argument is that the death of malls is a result of online retail. Is that correct?

We took this thesis as an opportunity to investigate the reasons for the decay of shopping centers in the US. What are the causes? What lessons can we in Germany learn from it? What possible measures can investors, operators, and retailers take to prevent a similar development? One surprising result of our inquiries: Online retail has not played a decisive role in the disappearance of American malls.

It is indisputable that shopping centers of all types are faced with some great challenges because stationary retail is itself under pressure. The pressure on retail is coming from different sources: a pure buyer’s (i. e. consumers) market and hyper competition, a lack of strict customer orientation, no clear positioning, and additional competition from pure-online retailers.

In addition to studying changes in retail, it is at least as important to observe fundamental trends, like wage and purchasing power developments, internal migration, urbanization, and the consequences of changes in the working world, to keep retail real estate profitable.

The following analysis is devoted to these latter aspects. It attempts, in a brief outline, to investigate some of the fundamental causes of mall death in the US.

Mall death in the US

In the American Midwest and South, former core regions of American industry, the number of highly qualified and well-paid jobs has disappeared over the past few decades due to structural changes in the economy. Producers and retailers from various industries sought ways to make mass products ever cheaper to produce. They therefore shifted industrial production to low-wage countries in the Asia-Pacific region.

Wal-Mart, a retail company, itself shares considerable responsibility for this development as it has endeavored to meet its company motto “Everyday low prices.” As a result, many high-paying jobs in the mining and metallurgical industry in the Midwest, and in the textile industry in the South, disappeared almost completely.

Quite a few of these lost jobs were replaced by ones with price-oriented retailers like Wal-Mart and, later, Amazon. Wal-Mart — with its low-wages — became the largest employer in the South and, in particular, the Midwest, which suffered most from the loss of industry. The new wage level in the regions is significantly lower than in the mining, metal, or textile industries. The average wage of an industrial worker is approx. $42,000 per year, while the substitute jobs pay approx.$23,000.

Over a longer period, an ambiguous picture has resulted. Wal-Mart’s low prices help to lower the cost of living. At the same time, price-oriented retailers like Wal-Mart and Amazon are suppressing the wage level, thus creating the very customers who are dependent on low prices.

It does not require great imagination to imagine the effects on purchasing power and consumption expenditure heralded by the income losses described above. The large-scale collapse of the middle class has led many shopping centers to close due to a lack of purchasing power. The losers in this development, who have become progressively poorer, simply cannot afford shopping as a leisure activity.

Mall death as market adjustment

Another factor that accelerated the disappearance of malls was their sheer number and the resulting oversupply. There were about 3,000 shopping centers in the US in 1960. By 2010, this had risen to 40,000. In this respect, a part of the story of mall death can probably also be seen as one of a market adjustment.

Qualified workers have migrated within the US to prospering coastal cities and to the sunny South, e.g. looking for jobs in other sectors. The different way of life in urban areas was not conducive to shopping malls. The disappearance of the malls is also linked to the crisis in the suburbs, which became manifest with the massive rise in fuel prices after the banking crisis.

The change in living habits in urban areas is a creeping, but steady, process. A big house on the outskirts, a big car, and permanent consumption of cheap goods manufactured in Asia is no longer the unconditional model. The search for more contemporary and intelligent lifestyles determines this trend. In the postindustrial inner city, residents turn to a more cultured life between lofts, health food stores, and permanent connectivity via smartphone.

This way of life and the enormously high cost of living in America’s urban areas led to a change in demand. The rise of Amazon and other digital business models like Airbnb is living proof. It is important to understand that the rise of Amazon trailed mall death in America more than it led to it. It is thus partly a consequence and an accelerating factor, but not a primary cause.

The rise of Airbnb, Uber, and other platforms is also attributable to the exorbitantly high cost of living in fashionable areas like San Francisco and Silicon Valley, New York, and Los Angeles. Even many relatively high-earning people can hardly afford to live in these places. Exploiting their property through platforms like Airbnb and Uber is a necessary source of income to maintain a person’s standard of living.

Airbnb is not a hotel company and Uber is not a taxi company. Both are simple, technology-oriented mediation platforms (brokers) that cannot exist economically without others’ private ownership. These platforms are helping destroy fixed and well-paid jobs as private individuals have unconsciously fueled a price war with their homes or cars, which may lead to a similar downward spiral that was the cause of the loss of industrial jobs in the American Midwest and South. This should not be overlooked. Let us now turn our attention to shopping centers in Germany, however.

Situation for shopping centers in Germany

If Germany had the same high level of shopping centers as the US, we would now have nearly 10,000 objects (400 of them malls). In fact, we estimate the number to be around 1,800, of which approx. 140 are malls, with around 260 power centers with more than 10,000 sq m of rental space. Around 1,400 of the properties are community centers measuring between 2,000 and 10,000 sq m of rental space.

It should also be noted that US malls and power centers have a significantly larger average sales area than their German counterparts, so the sales area in the US is in a completely different dimension: We estimate it to be approx. 920 million square meters, which is a per capita level of approx. 3.0 sq m per inhabitant.[1] Although the German retail trade differs from US retail through its significantly higher supply of space in inner cities, the per capita level in Germany is still less than 1.5 sq m in total.[2] This means the competitive pressures in the US are many times higher than in Germany.

As in the US, the number of new shopping center openings has also declined sharply in Germany. While new developments in the US have consisted almost exclusively of factory outlet centers in recent years (since 2012 about 10 per year),[3] the annual development in Germany is limited to a very few new power centers and shopping centers, as well as some extensions and modernizations of existing centers.

Specifically, GfK has reported the following figures for 2016: an inventory of 357 shopping centers and 258 power centers, as well as 600,000 sq m under construction/in planning until 2019. The 2017 figures are: an inventory of 358 shopping centers and 260 power centers, with 600,000 sq m under construction/in planning until 2020. Development has thus slowed faster in Germany than in the US. The result is that, as of now, there have only been a few isolated cases of vacancies and no large shopping center has ever permanently closed.

As previously described, purchasing power losses are responsible for declining consumption capacity in the US. The large average size of shopping centers and the high center density, combined with shrinking catchment areas and significant internal migration into selected, densely populated areas with a very high cost of living, has led to a diminished shopping center landscape.

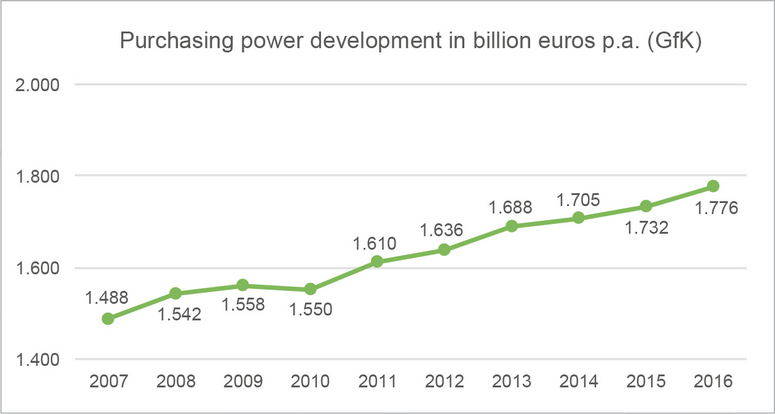

On the other hand, German purchasing power has grown unabated, a few crisis years notwithstanding, and has recently reached record levels. Although private consumption is growing faster than retail sales (2.1% compared to 1.5%), even brick-and-mortar retail stores are still in positive territory (2016: 0.8%).

Germany: Lower and middle-income classes have increasing incomes

The statistical situation in Germany is better than the impression the media sometimes give. The media frequently notes a rising income gap as a reason that a rising number of people are not benefiting from economic prosperity. Since, according to popular opinion, the middle classes in particular “feel” they have suffered from rising income disparities in Germany in the last 25 years, we will deal with the development of private household net income between 1993 and 2013 in more detail below.

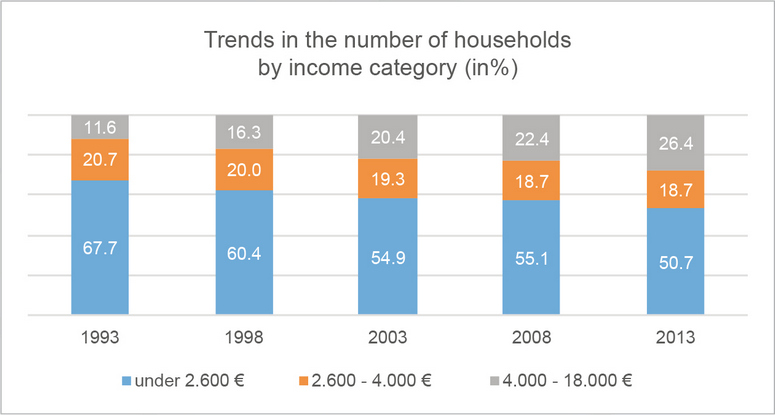

According to the income and consumption sample carried out by the Federal Statistical Office, the household income level of the middle class (between €2,600 and €4,000 net monthly) has remained largely stable. About one-fifth of households fall into this income category. The larger share of households with lower incomes (below €2,600), on the other hand, has clearly fallen in the last 20 years from around two-thirds to just around 50%.

The corollary is that there is a growing number of households with higher incomes. Their share rose strongly from 11% in 1993 to a good 26% in 2013. Even taking inflation (around 18% in 20 years) into account, the statistics show that both the lower- and the middle-income classes have progressed into the upper-income class. If an (inflation-adjusted) improvement had been denied the middle-income class, as the lower income class shrank, the middle class would have expanded significantly, but this has not happened. Instead, there has been a steady improvement in the income situation over the period since 1993.

No loss of purchasing power in Germany

Unlike in the US, Germany is experiencing neither a loss of purchasing power nor a negative development in incomes. Since a major part of the US problem can be traced back to domestic migration, which has impoverished whole regions, especially in the so-called “Rust Belt” between Chicago and Washington, but has also emptied rural areas as residents have migrated into dynamic metropolitan areas, a look at possible regional disparities is of great interest in Germany, too. The income and consumption sample provides interesting insights into peculiarities among cities and municipalities according to their population numbers.

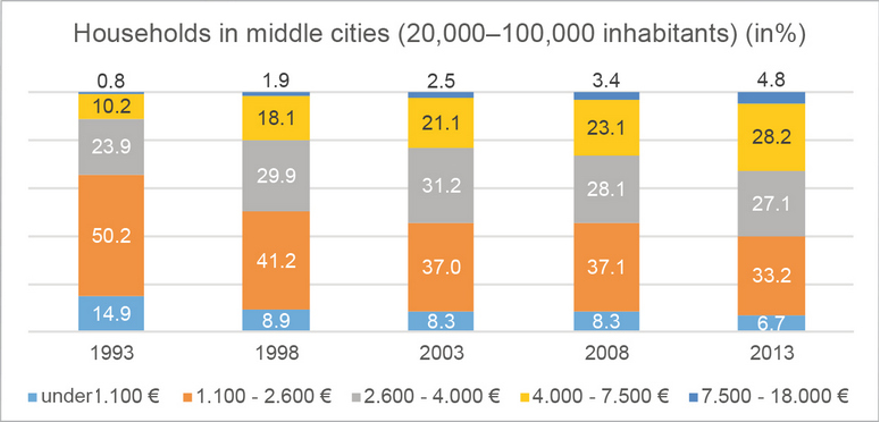

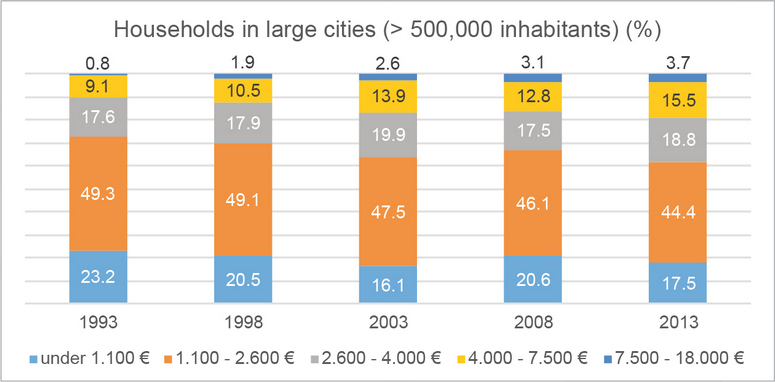

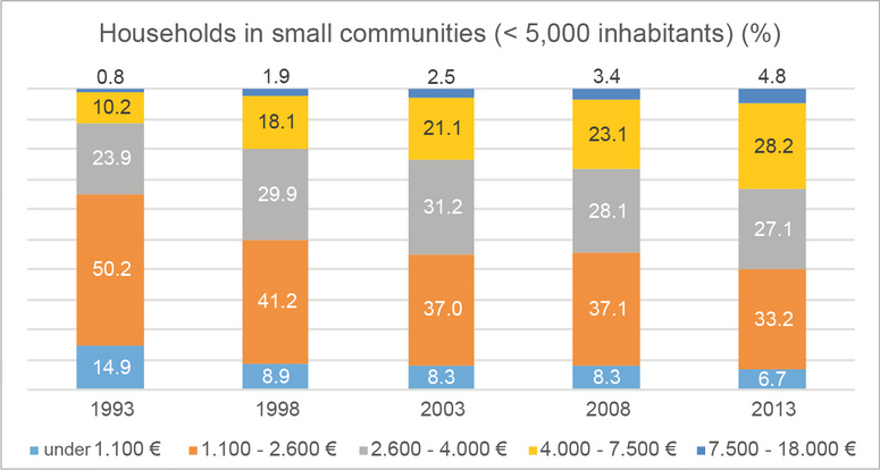

The finding of increasing proportions of the population falling in the upper income classes is valid in medium-sized municipalities (20,000 to < 100,000 inhabitants), as well as in large cities (> 500,000 inhabitants) and small towns (< 5,000 inhabitants). It is also clear, however, that the fall in the proportion of households in the lowest income level (under € 2,600) has been slower in large cities (11% between 1993 and 2003) than in any other place of residence. The best improvement among the lowest income level can be found in the smallest communities (-25%). The latter also boast the largest increase in middle- and upper-income classes. The absolute number of beneficiary households is correspondingly small, however, so this extreme percentage development is not actually relevant in practice.

Among the medium-sized cities so widespread, and therefore so important, in Germany (according to the BBSR there were 612 such cities at the turn of the year 2015/2016), the picture is once again pleasing: While the changes were largely in line with the federal average, the number of households in the lowest income classes has declined at an above-average rate in medium-sized cities.

Apparently, the inhabitants of smaller cities and municipalities can take advantage of the positive effects of economic development thanks to increased mobility better than is the case, in particular, in large cities. It must be assumed that the existing positive concentration processes in the metropolises will be partly dampened by negative agglomeration effects, which are probably mainly due to social issues.

The situation in Germany is thus completely different, and much more positive, than in the US, despite the somewhat weaker situation described above in its large cities and metropolises. In addition to the less dramatic competitive position in the retail sector, this is mainly due to the much more positive income and purchasing power situation among German households, which again shows no signs of growing disparities between the income classes. Online retail has a share of between 7 and 8% (including food) in both the US and Germany, so this factor should play no role in comparative analysis.

Mall death as in the US is thus not a threat to the future development of retail in Germany. On the contrary, the retail-related prospects for Germany are quite favorable, so the retail trade can concentrate on improving its service and customer-friendliness in the coming years. With meaningful and attractive multi-channel concepts, retailers can take advantage of the largely positive dynamic development in online retail for the stationary shopping experience and build a quality, adequate network even outside of major cities.

Clear positioning is indispensable

Against this background, retail, and in turn the retail real estate industry, has some homework to do that varies in difficulty depending on the sector. Hyper competition and a buyer’s market mean that basic tasks such as developing clear positioning, a 360° customer orientation, and appropriate brand strategies are the foundations for the future success of retailers with consumers. This also applies to the appearance and orientation of retail real estate. After all, retail real estate must support retailers in their brand management 100%.

Retailers that do not have brand strategies are inevitably caught up in pure price competition because they are interchangeable. Especially in the fashion field, the consequences of the absence of such foundations, such as increasing insolvencies among chain stores, could be observed in Germany in recent years. The development of a successful, multi-channel concept cannot make up for the lack of these basic principles. Without customer-oriented brand and a positioning strategy, the most elaborate multi-channel concept continues to be interchangeable across all channels.

Some retailers still define themselves through their purchasing power. This can be a hindrance under certain circumstances, since only purchasing power oriented to customer needs and the brand concept can ensure survival. Purchasing power alone does not help, since consumers expect that retailers and their sales concepts fit exactly to the daily lives and self-image of the target groups. This tailor-made benefit to each target group must be immediately recognizable to consumers. In Germany price has now become a hygiene factor—if offers are clearly positioned.

It is important for owners and operators of power centers and other types of shopping centers to obey the same rules. Only lively and profitable commercial locations ensure successful real estate. Owners and operators should therefore also seek close dialogue with retailers and they should all together ensure that consumer wishes are met.

[1] Source: eMarketer 2016, US retail sales in stores approx.$4.6 trillion, (2016). GfK estimates for average space output approx. $3,700/sq m pa = 1200 million sq m at approx. 325 million inhabitants.

[2] Source: GfK Geomarketing 2017

[3] Source: CoStar Realty, ICSC 2014

Follow ACROSS

![]()

![]()